THE TAX REGIME

SME SECTOR CAUGHT IN A WIDENING NET

Prashanthi Cooray explains why the revised social security contribution levy thresholds may create fresh financial and administrative stress

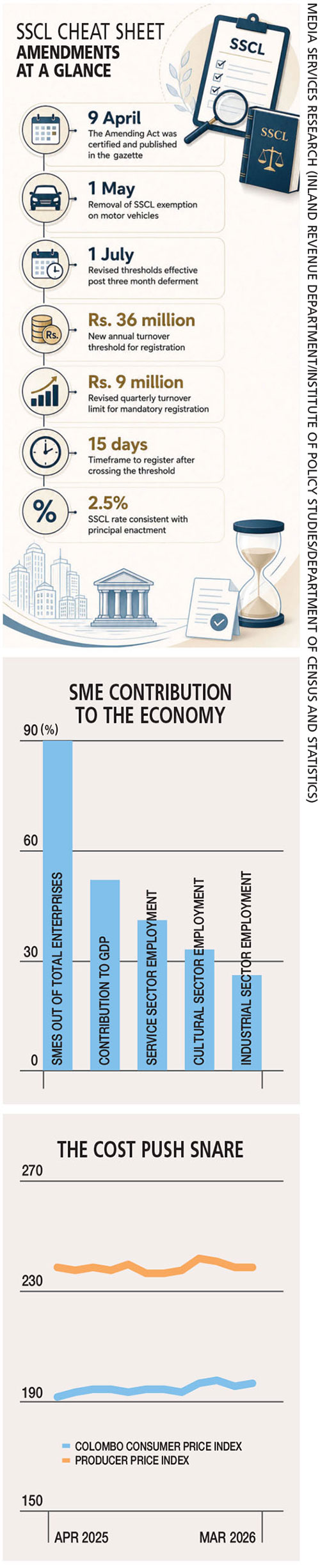

Sri Lanka’s latest amendment to the social security contribution levy (SSCL) may appear technical on paper but for many SMEs, it represents another layer of compliance pressure at a time when businesses are already stretched thin.

Under the Social Security Contribution Levy (Amendment) Act, No. 10 of 2026, the annual registration threshold for SSCL will be reduced from Rs. 60 million to 36 million rupees with effect from 1 July. The quarterly threshold will also fall from Rs. 15 million to nine million.

In practical terms, this means a larger pool of businesses will now fall within the SSCL net.

And while the government’s objective is clear – i.e. to widen the tax base and improve revenue collection – the move could burden SMEs that lack the systems, staff and the financial flexibility required to manage yet another tax obligation.

The SSCL was introduced in 2022 as a turnover based levy. Unlike income tax (which applies to profits), the levy is charged on turnover, meaning businesses are taxed regardless of whether they are realising healthy margins or not.

That distinction matters.

For many SMEs operating in sectors such as retail, distribution, hospitality and services, turnover can appear high while actual profits remain razor thin due to inflation, spiralling utility costs, rent and imported input expenses.

While headline inflation appeared manageable for much of early 2026, the underlying producer price index (PPI) remained stubbornly high, signalling that the cost of doing business never truly cooled.

As SMEs are forced to raise their prices to pass on these costs, their turnover inflates artificially. This pushes them over the new, lower Rs. 9 million quarterly threshold even if their sales volumes have remained stagnant – or declined.

This change also introduces a strict compliance timeline, requiring any person or entity whose turnover exceeds – or is likely to exceed – the stipulated threshold to register within 15 days.

For SMEs, this short compliance window could become an operational headache, as many still rely on manual bookkeeping or external accountants. Monitoring rolling quarterly turnover and ensuring timely registration adds complexity to businesses already grappling with rising costs.

There is also concern that the amendment may pull family run enterprises and growing mid-tier companies into a tax framework that assumes a level of administrative sophistication that SMEs lack.

For businesses already managing VAT, income tax, advance personal income tax (APIT) obligations and documentation requirements, the lower SSCL threshold adds to the cumulative compliance burden.

The amendment also revises the de-registration threshold.

Registered entities will only qualify for de-registration if aggregate turnover across four consecutive quarters remains below Rs. 36 million. This could create a one-way trap, where businesses that temporarily cross the threshold remain within the system even after their revenue streams head south.

Another complication lies in cash flow management.

Since SSCL is turnover based, businesses may need to pay the levy even when customer payments are delayed or receivables are pending. For SMEs dependent on credit cycles, that timing mismatch could intensify liquidity pressures.

To be clear, broadening the tax net is not inherently negative. In fact, Sri Lanka’s fiscal consolidation programme depends on stronger revenue mobilisation and improved compliance. And international lenders including the IMF have consistently encouraged tax reforms aimed at expanding the revenue base and reducing leakages.

But policy experts argue that implementation matters just as much as intent. Without stronger taxpayer education, simplified filing systems and practical transition support, the amendment risks overwhelming the very businesses often described as the ‘backbone of the economy.’

Many SMEs already tend to view Sri Lanka’s tax environment as being unpredictable, thanks to frequent policy changes, revised thresholds and shifting compliance requirements. That uncertainty can discourage formalisation and even incentivise underreporting among smaller operators trying to stay below registration thresholds.

The success of the SSCL amendment therefore, depends on whether Sri Lanka can balance revenue collection with the ease of doing business – because for SMEs, it comes down to coping with an increasingly complex regulatory burden.