TRIPLE BOTTOM LINE

THE BUZZ ABOUT SUSTAINABILITY

Gloria Spittel explains how the triple bottom line approach can benefit organisations

The concept of sustainability is about more than mere environmental consciousness. While much of sustainability focusses on the ethical use of the environment, the concept can encompass business procedures, strategies, goals and policies across an organisation.

Sustainable development is defined as meeting current needs without compromising the needs of future generations – as outlined in the paper Our Common Future, released by the UN Brundtland Commission, back in 1987. Environmental and social responsibility is also intrinsically entwined in this definition.

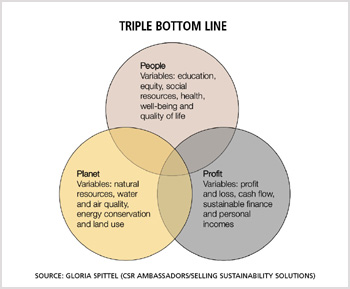

In business, defining and measuring the sustainability of procedures is an extremely tough task. To ascertain the parameters, the triple bottom line – a theory coined in 1994 – suggests three Ps: Profit, People and Planet. These three ‘bottom lines’ play the dual role of informing policy and measuring its effectiveness.

The theory suggests that measuring the three different, but related, bottom lines – the traditional bottom line, consisting of profits and losses (profit/economic), social responsibility of the company (people/social) and the company’s environmental responsibility (planet/environment) – offers companies an understanding of the true cost of doing business.

An organisation is sustainable when its operations have minimal negative impact on the local and global environment, community and society in which it operates; promotes employee welfare; and maintains ethical profit-making abilities.

Measuring organisational impact on economic, social and environmental dimensions is the first step towards enacting policies that would raise the sustainability profile of the company, by introducing preventive or corrective plans. However, utilising the triple bottom line as a measuring tool requires organisations to first set variables under each of the three dimensions that are related to the business, and are achievable.

Economic or profit sustainability mainly deals with traditional business measures, in terms of the flow of money – such as income, expenditures, taxes, consistent and profitable growth, shareholder returns and risk management. Usually, the goal is to sustain financial development through ethical means.

But the measure goes beyond traditional profit prerogatives. It combines environmental and social considerations, known as eco-economic and socio-economic, to determine the aggregate cost.

Eco-economic policies drive companies to work on resource and energy efficiency, while pursuing profits.

For instance, the materials and size of the physical company, and its contribution to the environment – e.g. waste products dumped into a river, which inadvertently causes harm to the environment; fauna and flora; and nearby communities. The socio-economic aspect of the profit bottom line considers the cost of underemployment, job growth and personal incomes.

The people or social bottom line measures social dimensions that are deemed important to a community or region. Far from being infrequent CSR projects, the variables that are established for the social bottom line are long-term policies that organisations seek to maintain in their operations.

These include equity and equal opportunity, by establishing diversity in the workplace; employee benefits, including health, social welfare and career development opportunities; and increasingly, a work-life balance. Other measures include promoting human rights, reducing community poverty, and accessing education and vocational training.

An example of a social bottom line is the fair trade movement, and activism against sweatshop labour in the world of business. The former is used to identify products that have been produced and traded in an environmentally and socially conscious manner, as opposed to sweatshop conditions.

However, this movement is not without criticisms, most of which revolve around the use of income from fair trade products to line organisational coffers, rather than provide a living wage to those involved in the manufacture of the product.

The planet or environment bottom line measures a company’s environmental footprint and viability of activities, which include the use of natural resources, energy consumption, waste disposal, land use and biodiversity management.

An example of this relates to the depleting resources of rare-earth metals, mined using cheap labour and utilised in the manufacture of technological products that are usually sold at a premium, as well as the cultivation of ‘fuel crops’ on arable land, for the purpose of producing biofuel (instead of food), especially in poor rural areas.

While some companies (especially small mom-and-pop shops) may find it unnecessarily complicated to fall in line with the triple bottom line, or think it is beyond their means to implement ethical policies, small, applicable and effective activities can assist them.

What is necessary for most organisations – regardless of size – is to realise that sustainability measures will reap benefits for all stakeholders, not only shareholders.

Sustainability in business is not an option, but a good choice for corporate success and societal well-being – it may even result in new product development. Put simply, ignoring it would be bad for business.

Certain values seem to have changed its form and got commercialised within a quick time period. Consequently, certain implied values have been pushed to a state of expressed conditions. Real values and morales have been replaced and taken over by commercial importance. Therefore, formerly valued aspects are losing its true meaning in today’s practical set up.

In a typical company’s annual report, TBLs are achieved in terms of content, technical terms and word power. Many annual reports express the company’s presence and adherence to corporate governance policies at strategy level, with the inclusion of audits and remuneration committees for transparency and employee rights.

However, we very well know that there are hardly any unbiased grievance policies and redress in place for employee harassment on behalf of employees in corporate offices. Even for many firms, social responsibility activities are carried out for the sake of disclosing in the annual report. May be there are a few firms which truly help a deserving employee’s family to live better and still not disclose it publicly.

TBL in true spirits should not be distant from the heart of corporate personality.

Nothing is free. There are hardly any profit making body that strives for triple bottom line (TBL) compliance without expecting any return, or at least goodwill. Organisations seem to have more priorities that will have to be achieved first, in order to look at the rules of the TBL, such as people, social, economic and environmental issues.

If TBL compliance is not viewed as a burden, or a rule imposed, many organisations can work and build together strategic and operational policies and practices that are in harmony with the society, people, and environment.

Vertical and horizontal integration, backward and forward integration with vendor management, tying up with customers and suppliers, managing service level agreements, merchandising and supply chain control and stakeholders such as pressure groups can be made feasible and continuously engaged through the TBL way.

If executed genuinely, TBL can assist a company to reach excellence.

An acronym for triple bottom line (TBL) – True Benefits Longstanding – there’s no better way to convey the purpose of triple bottom line straightforwardly.

When technically complying with TBL standards, some companies celebrate with big events. But when they do so, the celebration itself destroys the achieved TBL. The reason is that the celebrations end up consuming more energy, more carbon footprint, more waste and damage to environment, resources and even the exploitation of people.