INTERNATIONAL TRADE

SPOTLIGHT ON SUPPLY CHAINS

Samantha Amerasinghe assesses how geopolitical factors will impact trade

Persistent geopolitical tensions, high levels of debt and widespread economic fragility are expected to exert negative influences on global trade patterns this year. It follows that the outlook for global trade remains highly uncertain and generally pessimistic.

However, there are some bright spots too.

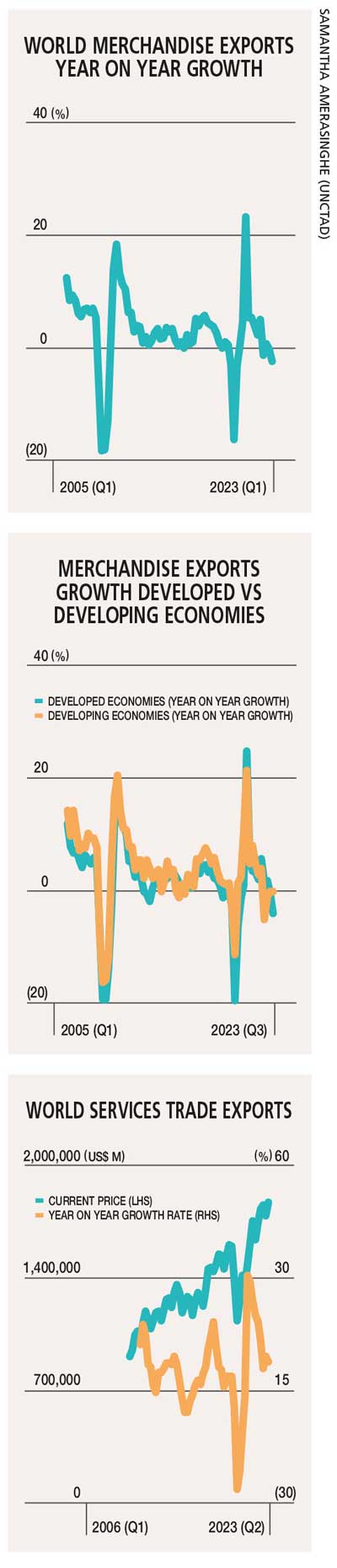

According to the latest Global Trade Update by the UN Conference on Trade and Development (UNCTAD), global trade in 2023 is projected to end five percent down compared to the previous year’s record level, shrinking by about US$ 1.5 trillion to below 31 trillion dollars.

Much of this can be attributed to trade in goods, which is expected to have contracted by nearly US$ 2 trillion (8%) in 2023. This decline was primarily driven by lower demand in developed nations, underperformance of exports in East Asian economies and a decrease in commodity prices.

Record levels of global debt are also driving the slowdown. This is because tightening financial conditions continue to heighten pressure on highly indebted governments.

Amid the largest surge in global interest rates in four decades, developing countries paid a record 443 billion dollars in debt service in 2022, according to the World Bank’s International Debt Report published in December.

Debt servicing costs ballooned last year and will most probably continue to do so. This is a clear indication that debt servicing will be a key driver of the trade outlook for 2024.

Global trade has also taken a beating from a wave of protectionist policies and restrictive regimes introduced in the name of national security or maintaining tech supremacy. Trade structures are no longer resilient to such shocks as restrictive measures have multiplied.

There’s been an uptick in trade restrictive measures and a lengthening of supply chains, particularly between China and the US. UNCTAD’s latest report highlights a substantial rise in non-tariff measures (NTMs) in particular, driven by a resurgence of industrial policies and the pressing need for countries to fulfil their climate commitments.

Surprisingly, recent trade regulations for climate action have identified over 2,300 climatic change-related NTMs affecting 3.5 percent of all potentially tradeable goods and covering 26.4 percent of global trade.

These factors have prompted countries to favour policies that support domestic industries and reduce reliance on foreign supply chains. Such inward looking policies are expected to continue to impede the growth of international trade this year.

But despite the somewhat grim outlook, there were a few positive trends last year.

For example, the services sector remained resilient and is likely to continue this year as well. The slight increase in trade volumes suggests resilient global demand for imports and a substantial US$ 500 billion increase in trade in services. And trade in services expanded by seven percent in 2023, thanks in part to a delayed recovery from the COVID-19 pandemic.

The key trade themes in 2024 will remain much the same as geopolitical tensions continue to impede global trade by making supply chain resilience a crucial factor. With risks remaining high for global supply chains, risk mitigation strategies such as supplier diversification, and ‘reshoring’ and ‘nearshoring’ – which were evident last year – will be prominent in 2024.

‘Friendshoring’ is a growing trend with many countries now showing preference for politically aligned trade partners. Trade concentration has also shown a marked increase with statistics showing an overall decrease in diversification of trade partners and indicating a concentration of global trade in major relationships.

Problems related to the Suez and Panama Canals will pose risks this year.

Around 12 percent of global trade passes through the Red Sea. And since this region is an important freight channel for oil, liquefied natural gas and consumer goods, bottlenecks in the Suez Canal could see inflation spiking. The implications for global inflation will depend on how long the blockages persist.

Although some businesses have already diversified their supply routes following the pandemic, this shock underscores the need for options.

The Suez and Panama Canal routes accounted for over half the container shipping volume scheduled between Asia and North America in the third quarter of 2023. And shocks pertaining to the Panama and Suez Canals are reminders that with climate change and growing geopolitical risks, supply chain instability is here to stay.

Downside risks to the global economy in 2024 and inflationary pressure are likely to persist. Interest rates are expected to stay higher for longer to curb inflationary pressures stemming from the monetary system.

However, long-term inflationary pressures from non-monetary sources such as the conflicts in Ukraine and the Middle East may also cause more volatility in oil markets.

This will drive inflation higher with broader implications at play – such as the potential fragmentation of the global economy and trade system – as sanctions avoidance could come to the fore.

Overall, it appears that negative factors will far outweigh positive trends in 2024 – it’s going to be another tough year for global trade.