BUSINESS SENTIMENT

INDEX AT AN EIGHT MONTH HIGH

Business sentiment takes a turn for the better ahead of the presidential election

Sri Lanka’s trade deficit contracted in August as imports continued to decline while the dip in exports of the previous month had largely recovered, according to data released by the Central Bank of Sri Lanka.

Import expenditure recorded a fall of 16.6 percent year on year and export earnings dropped by a fractional 0.4 percent year on year in August, which is mainly attributed to lower prices for major export categories.

Tourist arrivals increased by 24 percent in August over the preceding month while also narrowing the year on year gap.

However, workers’ remittances fell by three percent year on year to US$ 518 million in August; and on a cumulative basis in the first eight months of 2019, inflows declined by 7.6 percent in comparison to the corresponding period of the prior year.

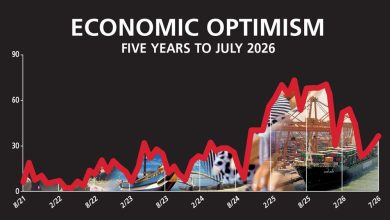

Notwithstanding these dynamics, the latest LMD-Nielsen Business Confidence Index (BCI) survey reflects a turnaround in sentiment – thankfully, for the better.

THE INDEX Business sentiment registered a noteworthy improvement in October with the BCI climbing to 102. This represents a substantial increase of 12 basis points from the previous month and is the highest score since February.

Elaborating on factors contributing to the uptick in sentiment, Nielsen’s Managing Director Sharang Pant says: “Impacted by the Easter Sunday bombings, Sri Lanka’s GDP recorded a growth rate of 1.6 percent – the lowest in 21 quarters. However, micro and macro indicators have steadily improved since then.”

He notes that “annual inflation has remained below two percent, driven by deflation in food prices; the rupee depreciated by three percent, largely on account of a strengthening dollar; exports continued to grow and registered three percent growth in the 12 months to 31 July; imports declined by 14 percent; and tourist arrivals are fast returning to normal averages.”

“The presidential election is also around the corner, leading to anticipation,” he adds.

SENSITIVITIES The economy and politics dominate the discourse on issues of national interest while the ease of doing business – vis-à-vis taxes, policies and inflation – emerges as the major concern in relation to the business environment.

“People don’t have adequate savings to purchase new things. Therefore, they tend to stick to the bare essentials,” a survey respondent asserts.

PROJECTIONS Pre-poll positivity seems to have been sustained in October as indicated by the surge in the latest BCI count.

And when the next survey is underway in the first week of November, we’d have entered the last stretch of the presidential race – and the index will therefore, reflect the corporate mindset at that time and thus be somewhat arbitrary.

So we will have to wait until the New Year to know where the index is really heading and to this end, Nielsen’s Managing Director explains that “election results will probably define the direction of sentiment in the ensuing three to four months.”

That said, we may then enter a new phase of ‘wait and see’ as the nation prepares for yet another election – this time to elect a government.