ECONOMIC OUTLOOK

Sri Lanka’s economic recovery may look reasonably good on paper but the reality on the ground is stark, with inflation appearing to have been only temporarily contained. While the crisis of 2022 was characterised by internal supply shocks, agricultural failures and a depletion of foreign reserves, the pressure is now a case of imported inflation.

FUEL PRICES IGNITE INFLATION PRESSURES

Prashanthi Cooray dissects the island’s fragile economic turnaround and explains how its surging oil import bill threatens stability

Higher crude oil prices and fuel import costs are filtering into the domestic economy, and pushing transport, logistics and wholesale prices up.

Because the country imports all its petroleum and holds less than a month of strategic consumption reserves, fuel acts as the volatile first domino that drives costs up, sparking inflation fears even when the local economy seems somewhat stable.

The primary trigger emerged in February, when escalating Middle East tensions sent shockwaves through the world’s energy markets. Volatility in the Strait of Hormuz disrupted supply routes and pushed the price of a barrel of Brent crude oil up to nearly US$ 120 on 29 April, driving freight costs through the roof.

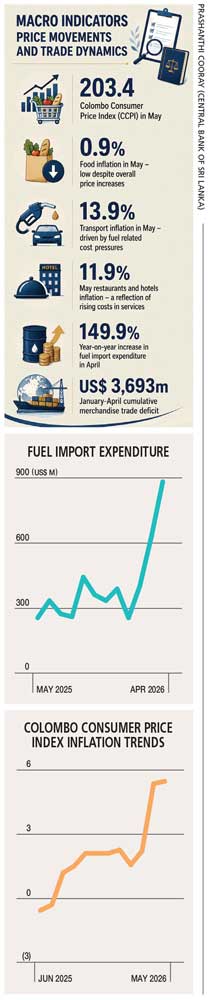

Consequently, Sri Lanka’s oil import bill surged by nearly 150 percent year-on-year to 886 million dollars in April – up from US$ 630 million in March. This shock was compounded by a weakening currency, with the Sri Lankan Rupee depreciating rapidly against the US Dollar by late May, climbing beyond Rs. 340.

Since oil is priced in dollars, the currency slide amplifies every shipment’s cost, creating a loop where higher import bills drain reserves and adds pressure to the rupee value.

This volatility has translated into domestic price adjustments through as many as five rapid revisions of the fuel pricing formula within three months. Retail fuel prices have surged by more than Rs. 100 a litre since March with octane 92 petrol reaching 434 rupees and auto diesel rising to Rs. 407.

More severe is the 56 percent spike in kerosene to 285 rupees, representing a long-term increase of nearly 550 percent since 2015, and directly affecting estate households and coastal fishing communities.

Treating these increases as technical adjustments overlooks their real impact. Fuel is the baseline of the national economy with effects that cascade through supply chains.

And this pass through effect is evident in official data.

Non-food inflation rose to 7.8 percent in May, driven largely by transport, which alone contributed 13.9 percent to year-on-year growth. And as fuel prices reset repeatedly, inflation expectations also adjust upwards, making each subsequent round of pricing more entrenched.

The result is a broader rise in inflation – with headline inflation reaching a 27 month high of 5.5 percent not long ago. The Central Bank of Sri Lanka has warned that inflation could climb to seven percent if fuel costs remain elevated, which is a reminder that the country’s recovery remains vulnerable to external shocks.

Households are already grappling with higher taxes, electricity bills and living costs. Rising fuel prices add yet another layer of pressure, leaving families with less in their pockets for everyday essentials.

The government cannot remain a mere observer of its pricing formula while pointing solely to international volatility. Although universal fuel subsidies are fiscally constrained under IMF commitments, a Rs. 57 billion temporary subsidy is currently absorbing part of the shock.

The Chairman of the Ceylon Petroleum Corporation (CPC) says that the true cost of importing and distributing diesel is around 750 rupees a litre with the state covering a considerable gap to maintain prices at the pump at Rs. 407. But this buffer is time bound and expected to last only till September, leaving an unresolved policy gap.

Beyond short-term relief, the challenge is structural: targeted support for vulnerable groups, stricter regulation of transport pricing and improvements in public transport are needed to prevent secondary price spirals.

On the supply side, diversifying procurement channels – similar to recent non-Middle East sourcing adjustments – could reduce our exposure to geopolitical shocks.

Sri Lanka’s experience reveals the hard truth that imported inflation is not an episodic risk but a recurring force in the economy. And unless stronger buffers are built against external energy shocks, every foreign disruption will arrive domestically… in full force.