DIGITAL ECOSYSTEM

FUTURE READY

Compiled by Yamini Sequeira

POWERING A CASHLESS ECONOMY

Avanthi Colombage reviews the state of play and future of digital payments

“Sri Lanka is firmly on a path towards digital maturity, progressing steadily alongside its Asian counterparts. The momentum in its digital jouney is real and consistent, even amid economic disruptions and natural challenges,” says Avanthi Colombage.

What stands out to her is the nation’s resilience and its continued openness to adopting innovations that can meaningfully enhance lives, while elevating the economic and digital landscape.

“Over the last few years, we have seen tangible progress in consumer awareness, a modernising banking ecosystem, expanding merchant acceptance and strong regulatory support. Contactless payments and mobile driven solutions are gaining widespread traction, reinforcing confidence in the direction of travel,” she adds.

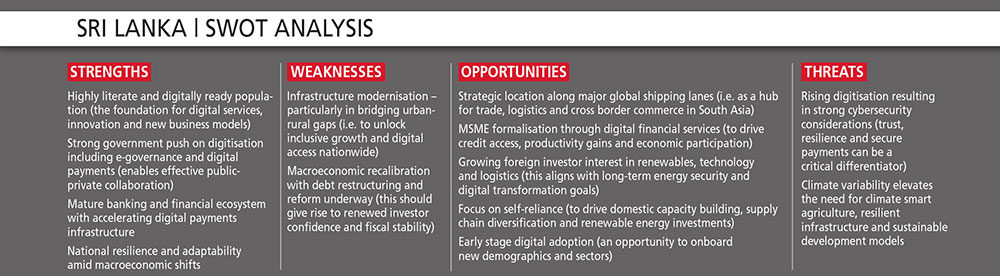

Equipped with an impressive literacy rate of 97.4 percent (which is a record high), the nation is uniquely positioned to accelerate digital payments adoption and unlock the full potential of a digitally enabled economy.

INCLUSIVE GROWTH Colombage notes that “a critical opportunity across emerging markets is bringing micro, small and medium enterprises (MSMEs) into the formal digital economy, particularly in high impact industries such as tourism. In Sri Lanka, this is already underway through strong public-private collaboration.”

“The most observed vulnerabilities – such as uneven digital adoption across segments, gaps in urban and rural infrastructure, evolving cybersecurity capabilities and the need for continued consumer education as digital usage scales – are being addressed as shared opportunities,” she assures.

As payment ecosystems scale, cybersecurity and fraud prevention naturally become areas of focus.

She observes that “presently, the country is progressing in line with global best practices, including the adoption of tokenisation to reduce exposure of sensitive data and strengthen consumer trust.”

“Furthermore, Sri Lanka demonstrates how emerging market vulnerabilities can be transformed into catalysts for growth when addressed early through collaboration,” Colombage explains.

DIGITAL ECONOMY Commenting on the most critical reform needed to accelerate cash to digital migration, she states that “Sri Lanka must accelerate the digitisation of all government payments – both collections and disbursements – on open, interoperable and low cost infrastructure, so that the state itself becomes the primary driver of cash to digital adoption across the economy.”

By ensuring that every citizen and micro business can receive, store and use money digitally through government touchpoints, this reform advances financial inclusion.

This will bring informal and underserved populations into the formal financial system, while enabling access to savings, credit and digital economic participation.

Interoperability is crucial to ensure that digital payments are convenient, accessible and scalable. When systems work together – allowing a consumer to pay any merchant on any platform, using any wallet or card – the entire ecosystem benefits.

Colombage explains: “If the ecosystem is fragmented, consumers face friction, confusion and inconsistency. Merchants may have to maintain multiple systems, increasing operating burdens. Costs rise across the ecosystem due to duplicated infrastructure. Trust erodes when digital payments don’t work everywhere and innovation slows because solutions must be rebuilt for separate networks instead of one unified environment.”

Over time, fragmentation creates a two speed economy: one segment benefits from digital convenience while another remains excluded.

“In a country where informal workers, SMEs, and micro entrepreneurs form the backbone of the economy, true inclusion means enabling individuals and businesses to participate fully, confidently and productively in the digital financial system,” she emphasises.

And she adds: “This requires simple, secure and affordable tools that bring everyday commerce into the formal ecosystem.”

Digital payments alone cannot drive inclusion; they must work hand in hand with digital identity, access to credit and strong financial literacy to build robust rails to the last mile. In her view, these three elements enable users to confidently adopt digital tools, build financial histories safely and unlock economic opportunity.

Accordingly, digital payments must be complemented by initiatives to improve digital literacy, expand credit access and establish secure digital identity systems. Designing an ecosystem that uplifts rural communities is the next major industry leap – and a powerful pathway to improving livelihoods.

The key will be to provide solutions that are simple and affordable, so that anyone, anywhere can participate without needing expensive devices or complex onboarding processes.

Over the next decade, cards, mobile wallets and account to account payments will coexist in far more seamless and interconnected ways than we see today. Cards will continue to play a foundational role, evolving beyond physical plastic into secure digital credentials powering all forms of payment.

SECURE PAYMENTS At the heart of this evolution is tokenisation, which replaces sensitive card details with a unique digital token, reducing the risk of fraud while enabling secure payments across cards, wallets, wearables and online channels.

Mobile wallets will continue to expand as the everyday interface for digital life, particularly among younger, mobile first consumers.

As Colombage points out, “in Sri Lanka, this shift is already visible. The country is now at 64 percent contactless penetration, more than doubling in only two years, with tap to pay becoming a way of life across consumers, merchants and businesses.”

“Account to account payments will also grow, particularly for government transactions, bill payments and recurring use cases. However, they’re most effective when combined with strong security, fraud protection and dispute management to ensure trust as volumes scale,” she adds.

In Sri Lanka, this multi rail future is already taking shape…

“Tokenisation will make digital payments far more secure across cards and mobile wallets while biometrics will simplify authentication for millions of users,” she asserts.

AI will become pervasive across the payments ecosystem, working in combination with tokenisation and biometrics to continuously enhance fraud detection, risk intelligence, security and increasingly personalised payment experiences.

Invisible, embedded and frictionless are – and will remain – the guiding principles for payments.

“From mobility apps and e-commerce to subscriptions, consumers expect speed, security and simplicity without needing to think about the underlying payment method. Yet, greater invisibility must come with stronger safeguards,” Colombage explains.

She continues: “This means modernised regulation, clear data protection standards and stringent consumer rights, all supported by the latest technologies.”

“The speed, scale and interconnectedness of the world have changed. Payments have evolved more in the last five years than in the previous 50. The acceleration of digital commerce, contactless payments, mobile wallets and real-time experiences has fundamentally reshaped how people and businesses move money,” she muses.

Even in a more complex world, the role of digital payments is clear: they support economic resilience, unlock new opportunities for businesses and consumers, and help countries integrate more seamlessly into the global economy.