GEM AND JEWELLERY INDUSTRY

Anchored by a heritage spanning over 2,500 years, Sri Lanka has long been synonymous with rare gemstones, exceptional clarity and the globally recognised Ceylon Sapphire brand. Today, the sector stands at a defining crossroads, balancing its illustrious past with the urgent need for structural reforms to secure its future.

SAPPHIRE STRATEGY

Compiled by Yamini Sequeira

BEYOND THE SAPPHIRE LEGACY

An enabling environment is key to unlocking potential – Akram Cassim

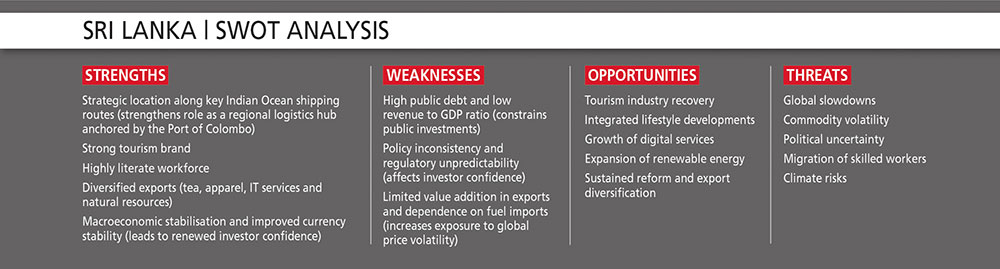

In 2023, Sri Lanka’s gem, diamond and jewellery exports reached approximately US$ 478 million, according to the National Gem and Jewellery Authority (NGJA), reflecting nearly 10 percent year-on-year growth from 435 million dollars in the previous year.

This performance appeared to signal renewed momentum, following years of global uncertainty.

“Unfortunately, this momentum proved to be fragile as exports fell sharply to around US$ 360 million in 2024, underscoring how sensitive the industry is to regulatory, fiscal and procedural shifts. This contraction highlights how quickly export performance can be disrupted by policy friction and administrative bottlenecks,” Akram Cassim notes.

Despite this volatility, the gem and jewellery industry continues to support an estimated 600,000 livelihoods across mining, cutting, trading, manufacturing and retail, underscoring its economic and social importance.

EXPORT MIX He explains that “Sri Lanka’s export mix is led by gemstones with blue sapphires accounting for the largest share by value, followed by diamond re-exports while loose coloured gemstones account for a substantial portion of exports.”

This reflects the country’s long-standing position as a trusted wholesale source of high quality gemstones to the global trade.

Meanwhile, finished jewellery remains a smaller but steadily growing segment.

“Blue sapphire remains our flagship gemstone and the backbone of our export identity. At the same time, the island has meaningful untapped potential to expand jewellery manufacturing and exports – building on our gemstone strengths while increasing value addition within the country,” Cassim states.

Simultaneously, tourism provides a strong platform to position Sri Lanka as the historic ‘Island of Gems: Ratnadeepa,’ he avers. Integrating gemstones and jewellery more strategically into the tourism experience through curated retail and mine visits can generate additional revenue alongside exports while strengthening global recognition of the country’s gem heritage.

GLOBAL DEMAND The international appetite for gemstones, especially Ceylon Sapphires, remains strong across key markets such as the US, Thailand, China, Hong Kong, Switzerland, the UAE and India.

“Buyers are increasingly discerning, prioritising provenance, certification, traceability and unique colour profiles. Our gemstones command premiums because of their clarity and pastel spectrum. Origin storytelling and ethical sourcing are now central to purchasing decisions,” Cassim adds.

Sri Lanka’s advantages are substantial: an internationally recognised gemstone identity, skilled artisans, ethical mining traditions and a heritage unmatched by most competitors.

He explains: “However, rival hubs such as Thailand, Dubai and Hong Kong outperform Sri Lanka in logistics efficiency, tax competitiveness and regulatory predictability. We lead in origin branding but lag in the ease of doing business – and that gap is becoming more costly every year. The challenge is not product quality but policy alignment with global best practices.”

As global trade becomes increasingly speed driven and digitally enabled, these structural disadvantages weigh heavily on Sri Lanka’s long-term competitiveness.

REFORM PUSH For the country to evolve into a serious jewellery manufacturing hub, several structural constraints must be addressed. Foremost among these is the free flow of raw materials.

Jewellery manufacturing depends on seamless access to gold, diamonds and gemstones. Competing hubs operate within long-term transparent frameworks that facilitate temporary imports and re-exports.

“By contrast, Sri Lanka’s policy uncertainty and administrative complexity discourage scale and long-term investment. Manufacturers need predictable systems. Without consistent access to raw materials, large-scale production is simply not viable,” he laments.

Gold import duties represent another critical constraint. High or unpredictable taxes inflate production costs and erode export competitiveness, particularly as gold remains the core input in jewellery manufacturing.

Cassim claims that “a regionally competitive gold policy is non-negotiable. Without it, value added exports cannot scale. Another major constraint lies in courier exports. As global jewellery commerce shifts online, Sri Lanka’s complex procedures for small value shipments hinder digital growth.”

Streamlined approvals, digitised documentation, faster customs clearance and better integration with payment systems are imperative. “Online trade is the future. But our systems are still designed for a pre-digital world,” he adds.

RETAIL ROUTE Here at home, the jewellery market remains diverse. Traditional family jewellers continue to dominate volumes – particularly in gold and bridal segments – while branded showroom chains and luxury boutiques are gaining ground in urban centres.

The growth of upscale malls and lifestyle destinations has reshaped consumer expectations. Jewellery is increasingly viewed as a luxury experience rather than a purely transactional purchase.

“Customers now expect premium environments, certification and transparent pricing. Retail is evolving from commodity selling to lifestyle branding. Tourist and diaspora purchases are also rising, reinforcing the industry’s shift toward higher value positioning,” he affirms.

Expanding jewellery exports and tourism linked sales would enhance foreign exchange earnings, and create skilled employment opportunities across the industry.

While no official statistics quantify informal trade within the gemstone sector, informal channels do exist. Cassim believes that establishing a supportive fiscal and regulatory framework – one that encourages formalisation and prevents sector activity from migrating overseas – should be a priority.

Policy liberalisation, streamlined regulations and practical incentives would help build a more transparent and competitive structure.

“Formalisation is a key priority. Without an enabling environment that attracts participants into the formal sector, we cannot fully unlock its economic potential. By improving the ease of doing business, we can expand the formal sector, strengthen revenue mobilisation and reinforce Sri Lanka’s reputation as a trusted source of ethically traded gemstones,” he emphasises.

DIFFERENTIATION Local designers play a critical role in differentiating Sri Lanka from mass-produced imports. Through bespoke craftsmanship and origin driven narratives, they generate higher value per stone and position the country as a design led jewellery destination.

“Our future lies in creativity. Not only selling stones but by relating stories through design. This shift from commodity to creativity is key to long-term sustainability,” Cassim reflects.

Looking ahead, he notes: “The gem and jewellery industry faces familiar risks – global inflation dampening discretionary luxury demand, high interest rates tightening liquidity, currency volatility and policy inconsistency affecting investor confidence. And yet, ample opportunities remain.”

“With the right-public private collaboration, we can move from being a gemstone exporter to a globally competitive jewellery hub. The one billion dollar target is achievable – but only if we modernise,” Cassim stresses.