CLIMATE ADAPTABILITY

Climate change affects various aspects of supply and demand in economies. Supply aspects include reduced agricultural and labour productivity due to higher temperatures, and increased morbidity and mortality rates.

What’s more, drought affects hydroelectric energy generation and agriculture while extreme weather events damage infrastructure.

THE ECONOMICS OF RESILIENCE

Why climate resilience matters Kiran Dhanapala elaborates

On the demand side, climate change can impact consumption (such as the greater use of air conditioning) and investment decisions in businesses, as well as economic growth in the long run.

Armed conflicts are disrupters to energy and transport sectors, and a systemic threat to energy transition especially in Asia. Fossil fuels are inflationary with supplies beyond our control.

When fossil fuel transport via shipping routes becomes a liability, coal often becomes the fallback commodity. And short-term energy security is likely to be put ahead of longer-term climate goals.

This is regressive – and the International Energy Agency (IEA) predicts a rise in fossil fuel demand through 2050. It will create increased climate instability and further shocks, which will affect growth.

Fiscal survival especially in Asia is better ensured by renewable energy and electrification. It also decouples energy security from geopolitical shocks. Policy needs to move investments into renewables such as lower costs for storage batteries.

Efforts to ramp up renewables are needed. The first international conferenceon transitioning away from fossil fuels that was hosted by Colombia and the Netherlands in April aimed to identify legal, economic and social pathways, to accelerate a fair, orderly and equitable transition away from fossil fuels.

Generally, GDP falls with increasing temperatures over time in both rich and poor nations, as well as hot and cold countries. But estimates on how this happens involve complex econometric estimation, emissions and climate scenarios among others.

The IMF has developed guidance on how to estimate the effects of slow-moving temperature changes on GDP and incorporate this into macroeconomic projections by countries. There are various econometric approaches that are vital for the assessment of long-term climate risks despite uncertainties and limitations.

Limitations include the non-inclusion of spillover effects such as trade, financial flows and migration, and uncertainties exist on the potential magnitude of climate impact on the economy.

But there are limits to econometric models such as the inability to account for global climate tipping points, which make loss estimates conservative.

There is continuing progress on estimating greater complexities. This includes the impact of extreme weather events not only in terms of temperature, and climate effects on revenue and expenditure, but also how climate policies – viz. adaptation and mitigation – will influence direct and indirect macroeconomic issues.

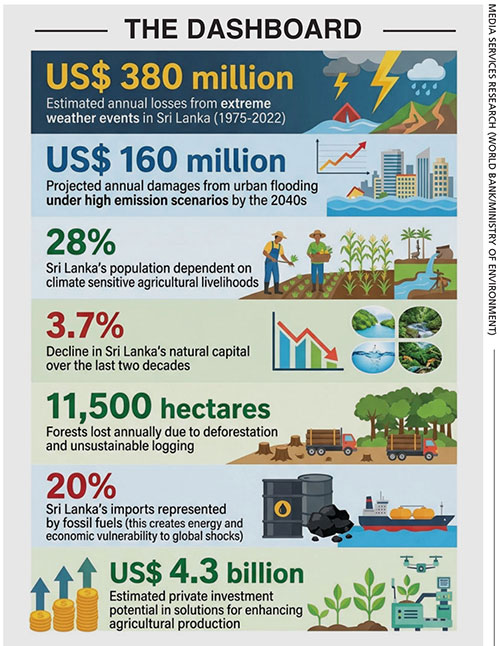

Before Cyclone Ditwah, the World Bank’s Sri Lanka Country Climate and Development Report (CCDR) 2025 identified key climate risks and solutions. It estimated potential economic losses between 3.3 and 3.5 percent of GDP by mid-century due to reduced labour productivity from heat stress, declining agriculture productivity, and more flooding in urban and rural areas.

The poverty impact is extensive – with increased rates of 1.7-1.8 percentage points. It also estimates that between 2025 and 2053, US$ 220 billion (4.3% of annual GDP) can be directed towards ‘no regrets’ investments for building climate resilience, and spurring economic activity and welfare. Of this, about 0.1 percent of GDP annually would be for targeted adaptation investments.

Another source of how climate change may impact Sri Lanka is the draft National Adaptation Plan (NAP) 2026-35, which estimates that over 19 million people will live in moderate or severe climate hotspots by 2050 with more than 81 percent of the population lacking sufficient adaptive capacity.

It estimates that adaptation requirements across all 13 sectors of the NAP would be over Rs. 297 billion (i.e. more than a billion dollars). Financing will need to be from various local and international sources, and include the private sector.

Post-Cyclone Ditwah, the World Bank’s Global Rapid Post-Disaster Damage Estimation (GRADE) report 2025 estimated the cumulative physical damage to be 4.1 billion dollars, which is the equivalent of around four percent of Sri Lanka’s 2024 GDP, and 0.48 percent of the estimated capital stock of buildings and infrastructure.

This is a preliminary conservative estimate that doesn’t include the total economic impact – e.g. indirect losses, cost of building back better and improvements for climate resilience etc.

Much of the estimated damage is for infrastructure (US$ 1,735 billion: 42% of the total damage), and transport, water and energy. This is followed by residential buildings (985 million dollars: 24% of the total) and agriculture (US$ 814 million: 20% of the total).