REAL ESTATE SECTOR

Sri Lanka’s real estate sector is showing signs of stabilisation and renewed confidence, following a prolonged period of volatility. Overall sentiment is gradually improving, underpinned by shifting buyer behaviour, the restructuring of financing conditions and broader macroeconomic stabilisation.

REALTY LANDSCAPE

Compiled by Yamini Sequeira

STANDING TALL AMID BARRIERS

Nayana Mawilmada offers insights into the momentum of the real estate sector

Putting this into perspective, Nayana Mawilmada says: “One of the earliest and clearest indicators of this transition has been the renewed momentum in land markets across the Western Province. Suburban land values in particular, are rising at a noticeably faster pace than those within core urban locations, reflecting changing affordability dynamics and evolving residential preferences.”

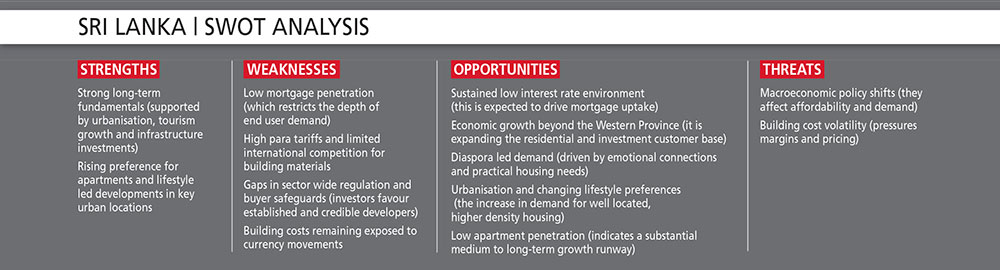

INVESTOR RESET According to the Real Estate Market Outlook Report 2025 compiled by LankaPropertyWeb, land prices in suburban areas of the Colombo District increased by an average 20 percent, outpacing the seven percent growth recorded in Colombo 1 to 15.

Across the wider Western Province, land values rose by 12 percent year-on-year.

Mawilmada notes that this divergence suggests that both buyers and developers are increasingly looking beyond traditional city limits, in search of relative affordability and long-term growth potential.

“This increase is driven mainly by limited land supply, some improvement in connectivity and rising affordability – partly due to lower interest costs – as well as the wider adoption of condominium style urban lifestyles,” he explains.

As land values firm up, these trends are beginning to filter through into the broader housing market, which is displaying clearer signs of balance. Demand is no longer dominated by a single buyer profile; it is increasingly spread across multiple segments.

“Current demand across the market is balanced between owner occupiers and investors. First time local buyers are becoming increasingly active, drawn by the convenience and lifestyle upgrades associated with modern apartment living,” he adds.

According to Mawilmada, investor participation remains healthy, “albeit with a clearer emphasis on rental yields and medium-term capital appreciation rather than short-term speculation.”

MARKET WOES While demand conditions are improving, supply side realities continue to present a more challenging picture: rising construction costs remain one of the most notable structural constraints facing the real estate sector.

“Factors such as high para tariffs and limited international competition for crucial building materials have pushed construction expenses above those of regional peers. Construction costs in Sri Lanka are higher than in Malaysia, which has direct implications for housing affordability, as higher costs are often passed on to buyers, constraining demand at the more affordable end of the market,” he claims.

The implications of elevated building costs extend well beyond residential developments. Mawilmada points out that other real estate linked sectors are similarly affected: “Investment in the hotel sector, for example, is severely hindered by high construction costs, which in turn translate into higher room rates.”

Meanwhile, the condominium segment is gaining renewed traction and stands out as one of the more resilient components of the market.

“Asking prices are firming up as buyer confidence returns and low interest financing improves affordability. Rental performance has been supported by strong occupancy levels and limited new supply in core locations. In this environment, condominiums are increasingly seen as a resilient asset class, blending liveability with investment potential,” he says.

Although concerns around unsold inventory often surface during phases of recovery, Sri Lanka’s structural context suggests that supply constraints remain intact.

Apartments account for around 14 percent of Colombo’s occupied housing stock – a figure well below that of regional peers such as Kuala Lumpur or Mumbai. This under penetration highlights the considerable long-term runway that still exists for vertical living.

At the same time, inventory levels in key segments are already tightening. Mawilmada elaborates: “In luxury developments, only around 400 units remain while mid luxury projects have roughly 1,000 units left across major schemes. Once this existing inventory is absorbed, new supply is likely to enter the market at higher price points as replacement costs rise.”

Another stabilising influence on demand is the contribution of Sri Lankan expatriates. While domestic buyers continue to account for roughly 70 percent of transactions, expatriates represent a meaningful 20-30 percent with interest originating from the Middle East, Europe, North America, Australia and Canada.

“This diaspora cohort reflects not only investment interest but also emotional motivation. Many are driven not merely by financial returns but a desire to own a piece of home,” he muses.

EASY LOANS Financing conditions have played a pivotal role in converting latent demand into active transactions. Mawilmada explains: “Affordable financing is helping both end users and investors make prompt decisions.”

“Banks are increasingly offering higher loan to value ratios and long-term fixed rate loans of up to 20 years with some lenders factoring rental income into repayment capacity. These innovations have broadened access, particularly for first time buyers and younger households,” he adds.

From a policy perspective, the broader environment has supported the recovery, although targeted reforms remain necessary. Urbanisation trends continue to shape long-term development strategies. Colombo and other city centres remain pricing anchors, supported by sustained demand and limited land availability.

For the time being, most large developers remain focussed on Colombo and the Western Province. Yet, there are growing indications that expansion into tier two and three urban centres is approaching. However, infrastructure has yet to keep pace with population expansion.

“We are at least five years away from any major shift in commute patterns – probably more,” Mawilmada notes, pointing to the slow evolution of mass transit initiatives.

“Until such infrastructure matures and commute times drop dramatically, core locations in cities will retain much higher pricing and suburban expansion of multifamily housing will be constrained,” he affirms.

The lack of supporting infrastructure beyond the city of Colombo – such as sewerage networks, for example – compels developers to invest in bespoke wastewater treatment systems, adding to project costs and constraining expansion.

“Rising incomes, land values and evolving lifestyle preferences suggest that demand will gradually extend beyond the Western Province; it’s merely a question of time,” he states.

Having recalibrated through the hyperinflation cycle, the property sector continues to be viewed as a hedge against long-term inflation and currency risk, thereby reinforcing its role as a core component of Sri Lanka’s evolving investment landscape.