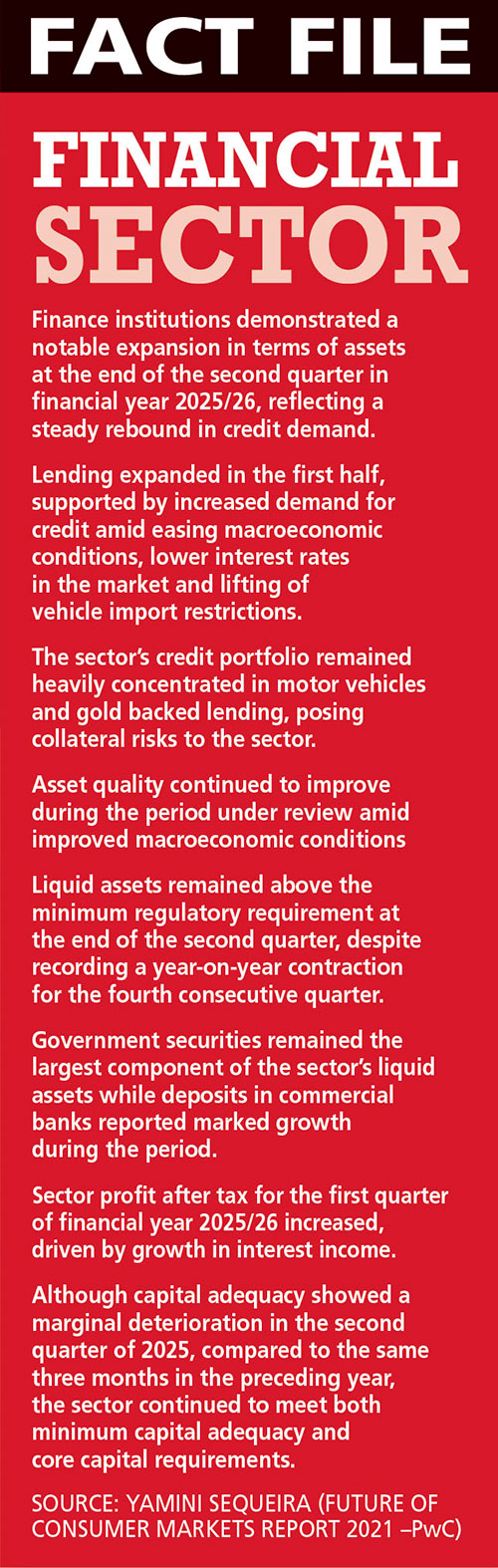

NBFI SECTOR

Sri Lanka’s non-bank financial institutions (NBFIs) are entering a new era. Emerging from one of the most turbulent economic periods in history, the sector has moved into a phase of measured expansion, innovation and structural rethinking.

GROWTH REIMAGINED

Compiled by Yamini Sequeira

MULTIPLE LEVERS OF GROWTH

Conrad Dias identifies trends and game changers in the financial sector

“The year was favourable for the sector. Following the economic crisis, we’ve seen the benefits of stability and lower interest rates, which have enabled institutions to plan ahead – something we were unable to do during the high interest regime,” says Conrad Dias.

For years, most NBFIs relied on short-term funding models due to the volatility of rates and liquidity pressures. Today, the sector is shifting gears.

He continues: “Many non-bank financial institutions and banks have begun issuing long-term debt instruments such as debentures. This reflects a sign of confidence in the long-term stability of the sector and a clear intention to grow.”

RENEWED CONFIDENCE Asset quality has markedly improved, especially within the leasing segment – a cornerstone of NBFI business.

“The NBFI sector has long been anchored to vehicle financing, from two-wheelers and three-wheelers, to commercial and industrial vehicles. With the lifting of import restrictions and a more stable US Dollar, vehicles are entering the market again. This has helped companies grow their portfolios and manage their non-performing loans (NPLs), thereby stabilising their books,” he explains.

And indeed, the numbers support this shift: once in high double digits, NPLs have fallen to single digits across the sector. Higher gold prices have also made it a strong growth driver.

Dias notes: “Most NBFIs are seeing their gold loan books doubling in size. With world prices firming up and local pricing stable, gold loans have become one of the safest and most profitable lines of business.”

FINANCIAL INCLUSION While the sector’s future looks promising, its real strength lies in its reach.

“Non-bank financial institutions play a critical role in financial inclusion; they serve approximately two million borrowers and three million savings accounts, compared to banks that largely focus on corporate and commercial clients,” he emphasises.

Dias cites data from the Credit Information Bureau (CRIB) to back his claim: “The majority of CRIB reports are pulled from NBFIs, which reflects the granularity of our customer base. We reach individuals in rural and semi-urban areas who would otherwise have no access to credit.”

MSMEs remain the backbone of Sri Lanka’s economy and the NBFI sector has been an essential partner in their growth. The willingness to extend soft collateral loans has been a key enabler for small businesses and micro entrepreneurs.

“We lend against soft collateral, unlike banks that rely heavily on hard assets, especially for MSMEs. Until our credit culture and alternative data availability matures, this flexibility will remain essential for SME growth,” he asserts.

A broader concern, he cautions, is access to finance for the underbanked. “Most Sri Lankans have a bank account or a debit card but that does not imply financial inclusion, as many don’t have real access to formal credit. However, NBFIs fill this gap,” he maintains.

The sector also faces another social challenge: tackling the informal money lending market.

“Unregulated lenders charge exorbitant rates – sometimes as much as between five and 10 percent a day. Many small borrowers prefer this option because they need short-term loans. The sector must create a formal regulated solution for this segment,” Dias urges.

However, he believes much more can be done to support this base.

“Ample opportunity exists in this segment. Although NBFIs have come far, we can do more to empower SMEs and micro enterprises,” he muses.

TECH IMPERATIVE Looking ahead, he identifies technology as the game changer for the NBFI sector.

“Technology will redefine how we reach customers, especially in rural areas. Fintech, digitalisation and AI will transform service delivery, risk management and decision making,” he adds.

Dias believes that technology is now both accessible and affordable. He explains that “technology has been democratised and demonetised – which implies it’s available to everyone and affordable for anyone. This will drive the next leap in productivity, customer experience and financial services transformation.”

Yet, with greater digitisation comes greater risk. “Cybersecurity will be one of the biggest challenges. We’re moving towards artificial intelligence driven cyber threats, not only human led attacks. The entire financial sector must elevate its defences several fold,” he cautions.

In his view, sector consolidation – which is another major trend – is yielding clear benefits: “Consolidation brings efficiency. Expanding beyond Sri Lanka is no longer optional for growth oriented NBFIs. Every Sri Lankan enterprise – not merely NBFIs – must look outside. We’re a population of 22 million; we must scale up and beyond our borders.”

REFORM OR PERISH Despite signs of recovery, Dias believes the wider financial sector requires structural reform.

He cites India as an example with its variety of banks encompassing export-import facilitation, development, microfinance and payments, each catering to a specific segment.

“This specialised structure ensures that every segment of the economy receives the right financial support. Specialised banks could address long-term funding gaps and drive development financing,” he explains.

However, Dias urges: “Our development banks have shifted towards retail and commercial lending. Their appetite for long-term projects has disappeared because short-term lending is easier and more profitable. We need to bring that balance back.”

FUTURE READY For Sri Lanka’s economy to accelerate, he believes that the following actions are essential: segmenting and restructuring the financial system.

He elaborates: “Each sector – agriculture, exports or microfinance – needs its own dedicated support structure. What’s more,we must move beyond traditional industries and support startups – particularly tech led startups, as that’s where the next wave of growth will come from.”

Moreover, he explains that “we must build a tax culture that fosters trust. People need to see their tax rupees being put to good use. When that happens, digital payments and formalisation of the economy will naturally follow.”

Dias also sees environmental, social and governance (ESG) as a growing priority.

“Whether we like it or not, ESG is now a corporate responsibility. With new sustainability reporting standards, especially for listed companies, it’s no longer optional. Today, perhaps 10 percent of lending is ESG linked and by 2030, this will rise to 50 percent,” he reiterates.

He concludes: “We’re past the stage of survival. This is the time for transformation – for smarter regulation, technological leapfrogging and a shared vision of inclusive growth.”