THE BIG PICTURE

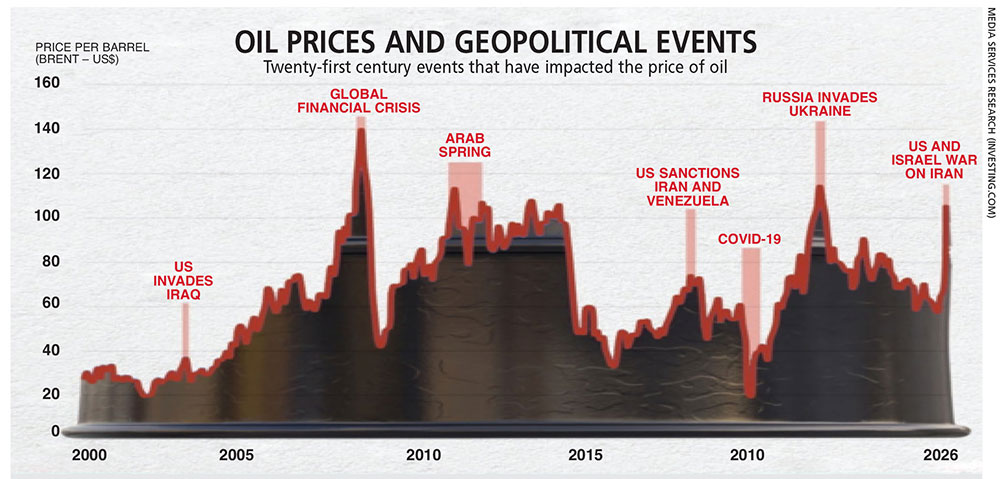

The price of oil has been the subject of extreme volatility since the US and Israel embarked on their war on Iran on 28 February – perhaps like the world hasn’t seen before: every utterance – especially by POTUS! – has sent the price of oil on a spiral in one direction or the other; and there have been times when the price of Brent crude threatened to surpass its all-time high during the global finance crisis back in 2007/08.

CONTOURS OF PETRO WARS

Reality check on how the price of oil is affecting the world

Of course, the price of black gold affects the entire world indiscriminately, although it is the poor and poorer nations that bear the brunt of the resulting mayhem. But when supply chains are disrupted, both the rich and poor feel the pain.

As the IMF’s Director of the Middle East and Central Asia Department Jihad Azour cautions, “the global economy is facing a broad and deep shock, as disruptions linked to the Middle East war severely affect energy markets, commodity supply chains and financial stability.”

In recent weeks, the price of a barrel of Brent crude oil surged above US$ 100, peaking at 118 dollars before easing following the announcement of a ceasefire. And gas prices have climbed by some 60 percent, exceeding the spike in the aftermath Russia’s invasion of Ukraine.

On 23 April – amid the diplomatic impasse between the US and Iran – the price of Brent crude stood at 106, pending any form of finality in regard to Iran, the Strait of Hormuz and Lebanon. For the record, the price of a barrel of oil before all hell broke loose was US$ 72 – i.e. more than 50 percent lower.

The disruption has extended beyond oil and gas: around a third of the world’s fertiliser transits the Strait of Hormuz; and it follows that surging energy and commodity prices are feeding directly into higher food costs and security.

“Sri Lanka is in a stronger position than it was at the height of its economic crisis to support citizens affected by rising energy costs; but it must continue its reform path to secure long-term stability, a senior International Monetary Fund official said in Colombo not long ago…

Krishna Srinivasan – who is the Director of the IMF’s Asia and Pacific Department – affirmed that Sri Lanka has made significant progress over the past three years in strengthening its fiscal position, particularly by boosting tax revenue as a share of GDP.

He noted that these improvements have helped the country gradually rebuild its fiscal buffers, adding: “Sri Lanka is better placed to provide support to the people who have been hurt by this energy shock.”

However, Srinivasan noted that Sri Lanka shares vulnerabilities with many other Asian economies due to its reliance on imported oil and gas, thereby exposing it to energy price shocks.

The reality therefore, is that we are likely to be facing more uncertainty and some strife this year.