LMDtv 3

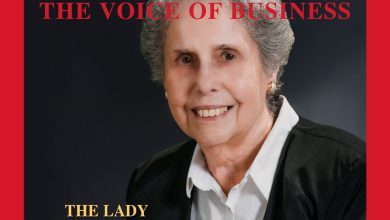

Despite the turbulent waters that Sri Lanka has been navigating in the past, the insurance sector has always been steadfast and resilient. “Irrespective of the economic activity in a country, insurance will always be resilient in terms of mitigating financial risk,” said the Chief Financial Officer of Union Assurance Himani Weerasekera, during a recent LMDtv interview.

Balancing profitability and expenditure is challenging during economic crises but the sector has remained strong.

She elaborated: “Revenue has increased annually, so we didn’t experience a significant impact in terms of managing costs. However, an area that we look into is managing the fund. When there are high interest rates, we invest primarily in bonds and bills to manage our capital adequacy ratios.”

“As we invest in high yields, we’ve managed to service our policyholders and shareholders alike in the long term,” she added.

Weerasekera continued: “Profitability is not only about expenses; it’s also about the investment income and revenue we receive. Insurance companies have been able to establish long-term investment plans to safeguard funds, which is one of the reasons that profitability has not been impacted too much.”

Although Sri Lanka’s insurance sector is performing well, it has one of the lowest penetration levels in the region.

She noted: “Penetration hasn’t shown much progress over the years and it’s currently less than two percent. Despite economic progress in indicators such as GDP and per capita income, the distribution of wealth among the population is unequal, and we still see about a third of the people living below the poverty line.”

“Coupled with the standard of living, this impacts consumption and demand, which in turn results in hindered progress,” she added.

There are other factors such as awareness as well, as Weerasekera explained: “It’s challenging to go to rural communities that aren’t tech savvy and have comparatively low literacy levels. They find it difficult to understand why insurance is a necessity.”

Furthermore, Sri Lankans are very family oriented. “While this is good, the flip side of it is that we’re dependent on our families,” she said.

Weerasekera added: “Although we have an ageing population, it’s evident that elders like to depend on their family members – and therefore, they don’t see the need for insurance.”

She also outlined how many people don’t earn on a monthly basis and don’t have regular incomes. “Products such as life insurance require a long-term commitment – it’s not something you can purchase for only a year. So people find it difficult to stay committed and seek short-term solutions – they don’t want to think that far,” she asserted.

On the positive side, the insurance sector has also seen widespread innovation in the form of product development. Weerasekera pointed out that “traditionally, insurance was seen as a protection mechanism; but now it is far more than that and people are looking for different types of cover.”

She continued: “They would normally opt for basic life cover but today, customers can include other aspects such as healthcare, disability and even pension plans. People want tailor-made solutions these days and companies are looking to offer more personalised products.”

The younger generations are also making an impact, she revealed: “For instance, millennials and Gen Z use social media platforms more than anyone else. They like to work on apps, use online platforms and are very aware of what’s happening because of the accessibility to information.”

“They also like to read reviews and comments. So I think those platforms can be used extensively to cater to these segments,” she opined.

The insurance sector has remained resilient and stable, and continued to perform consistently year on year. “And with the island’s economic recovery and economic activity picking up, sector performance is expected to improve too,” she concluded.