UK INFLATION RATES DOUBLE

The annual UK inflation rate more than doubled in April, as a rise in energy and clothing costs drove prices higher.

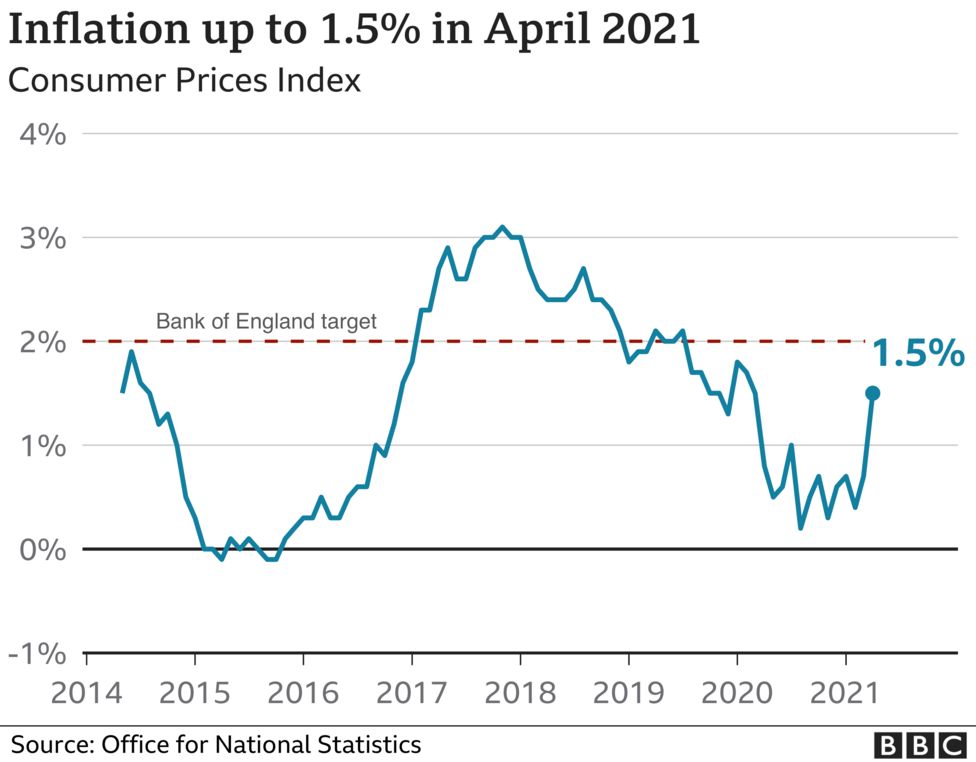

The jump to 1.5% in April from 0.7% in March, means consumer prices are rising at their fastest rate since March 2020 at the outset of the pandemic.

The sharp increase largely reflected a jump in prices from low levels a year ago at the start of the pandemic, the Office for National Statistics said.

Higher oil prices also pushed up petrol prices, it added.

According to the ONS, inflation climbed as lockdown restrictions were eased and shops reopened on 12 April. The rise in clothing and footwear prices reversed an unusual fall in February.

Meanwhile, gas and electricity prices rose sharply after the default tariff cap was increased compared with a cut a year earlier.

Hannah Audino, economist at PwC, said she expected inflation to continue to rise as lockdown restrictions eased and the economy continued to reopen “allowing consumers to unleash some of their excess savings”.

“Recent survey evidence suggests that the share of households who plan to spend some of their savings has increased in recent months, as the vaccine rollout boosts confidence,” she added.

April’s inflation rise had been predicted by economists, but there are concerns that soaring inflation this year as the global economy recovers from the pandemic could push central banks to raise interest rates.

‘Bottlenecks’

Earlier in May, fears about rising inflation in the US hit financial markets after consumer prices recorded their biggest annual jump since 2008.

High government spending on Covid support programmes, coupled with a build-up in consumer savings, have driven prices higher, says experts.

Liz Martins, senior economist at HSBC, said that it looked like UK inflation would go above the Bank of England’s 2% target, although this was “not too much of a worry for the Bank”.

“Their view is that they need to keep inflation sustainably around 2% two to three years out from now, so the short term overshoot won’t worry them too much, if it does prove temporary – and that’s where opinions really seem to diverge,” she told the BBC.

Many central bank governors, particularly in the US, are saying that the rise is due to bottlenecks in the aftermath of the pandemic which will go away, Ms Martins said.

But some people, including Bank of England chief economist Andy Haldane, say higher prices could stunt the recovery and that the Bank may need to raise interest rates to cool things down.

Laith Khalaf, a financial analyst at AJ Bell, said that the rise in prices was “in key areas where it’s hard for consumers to control spending, namely transport, clothing, and household energy”.

“At current levels, inflation is nothing to fret about, but there is rising concern that the fiscal and monetary response to the pandemic has sown the seeds of an inflationary scare further down the road,” he said.

He said the Bank of England has made it clear it will tolerate inflation above its 2% target without “pulling the trigger” on interest rate rises.

“However, if inflation looks like it’s going to get a significant foothold, markets will take matters into their own hands and raise borrowing costs across the economy,” he said.

Two weeks ago the Bank of England said that UK inflation is heading above its 2% target and is expected to hit 2.5% at the end of 2021.

That is due to a rise in global oil prices and the expiry in September of Covid emergency cuts to value added tax (VAT) in the hospitality sector, as well as comparisons with the pandemic slump of 2020.

The Bank thinks inflation will then slip back to 2% in 2022 and 2023.

Bank of England governor Andrew Bailey said on Tuesday that so far there was no strong evidence that higher prices paid by manufacturers were feeding through to consumer prices.

However, he said the Bank “will be watching this extremely carefully” and would take action if necessary.

So a return to more normal levels of inflation was always likely as the global economy slowly started to re-open.

Clothes prices, for example, contributed to the rising cost of living not because they were rising by much but because they were no longer falling.

What’s spooked markets recently is the risk of inflation coming down the pipeline.

In a literal sense it already is: the price of oil has been rising in anticipation of a global recovery, pushing up petrol and household bills.

Last week, markets took a knock fearing that the rising cost of raw materials would force the Bank of England to raise interest rates from their rock bottom official level of 0.1% sooner than anticipated to stop inflation getting out of control.

The Bank of England Governor Andrew Bailey has twice spoken publicly to play down that anxiety, saying on Tuesday that he had not yet seen strong evidence of those rising costs being passed through to consumers.

But Wednesday’s figures for what manufacturers are paying for raw materials show a rise in input prices – what manufacturers pay for raw materials – of 9.9%.

That’s the fastest rise in four years and faster than most economists expected