THE LITMUS TEST

SPHERE OF CORPORATE INFLUENCE

The architects of biz success grapple with the inevitable volatilities that bedevil an economy in transition

The all but ambiguous environment for business in present-day Sri Lanka is exemplified by the 2015/16 edition of the LMD 100, with performance indicators reflecting a mixed bag of fortunes and misfortunes. Regrettably, regime change and ensuing policy initiatives – if one could call it that – have only added to the sense of uncertainty among corporates, investors and other stakeholders of the domestic economy… thus far, at any rate.

While the private sector is often touted as being the engine of economic growth, it has borne the brunt of the fallout from ad hoc and inconsistent fiscal policy direction in the recent past.

The seemingly endless but now largely concluded saga surrounding the Value Added Tax (VAT) rate hike is perhaps the worst example of inept fiscal policy management, with delays in its implementation costing the nation an estimated Rs. 80 billion – that’s more than the annual income of Sri Lanka’s leading private sector bank. Speaking at a business forum in November, the Minister of Finance reportedly warned that Budget 2017 would be a ‘rude wakeup call’ for the private sector, “which should now end their (sic) wait and see policy.” And while the full impact of the government’s recent fiscal policy brief will only be known in the weeks and months that lie ahead post implementation and evaluation, the general sentiment is one of yet another round of belt-tightening on the part of corporates. The wakeup call therefore, may not be heeded by the corporate elite.

Despite the many issues that hang in the balance, Sri Lanka’s foremost listed entities that grace the latest LMD 100 rankings continue to look to the future, remaining cautiously optimistic about the operating environment they may have to face. Having navigated the fluctuating tide of the nation’s economic growth programme in years past, they continue to set the bar even higher for those attempting to follow in their footsteps.

LEADERBOARD A Sri Lankan corporate powerhouse reclaims the LMD 100 title this year, ahead of another highly regarded diversified conglomerate that crossed the finish line first in 2014/15.

Meanwhile, an oil-palms-centric corporate with offshore links and a financial services giant trail somewhat closely behind, making their presence felt on the 2015/16 Leaderboard.

John Keells Holdings (JKH) was ranked No. 1 in eight of the first 10 years of The LMD 50 (the pioneering precursor to the LMD 100), only to be surpassed by Sri Lanka Telecom (SLT) – a partnership between the Government of Sri Lanka and Malaysian telecom giant Maxis, which went public in 2003.

SLT in turn helmed the rankings for four consecutive years, before surrendering its place at the top of the ladder to a petro giant from neighbouring India: Lanka IOC was The LMD 50’s numero uno until 2009/10, with its reign lasting three years.

And Hayleys, which was runner-up to JKH in many of the early years – and pipped the latter to the winning post in 1995/96 and 1996/97 – also raced ahead of SLT and Lanka IOC in 2010/11, to occupy the podium’s second place.

In the latest LMD 100 rankings, JKH takes the No. 1 spot, while Hayleys surrenders its leadership mantel to receive the runner-up title. Bukit Darah stays put in third place and is followed by Commercial Bank of Ceylon (ComBank). Dialog Axiata rounds off the top five, climbing one spot higher on the LMD 100 ladder.

The remainder of the Leaderboard consists of CT Holdings (No. 6), Cargills (Ceylon) (in seventh place) and Lanka IOC (No. 8), as well as Hatton National Bank (HNB) and SLT who are ranked ninth and 10th respectively.

REVENUE STREAMS Aggregate revenues of the island’s 100 largest quoted businesses reached Rs. 2,309 billion in 2015/16, reflecting an annual growth of eight percent. This increment in combined annual earnings only exceeds the official rate of inflation in the period under review by a small margin.

In the preceding financial year, the LMD 100’s cumulative turnover turned up by five percent, with inflation being in the low single digits.

Meanwhile, over a third (35 to be precise) of the LMD 100 registered annual revenue streams in excess of 20 billion rupees, which is a slightly higher number than in 2014/15. The three highest ranked corporates (JKH, Hayleys and Bukit Darah) also surpassed the 80-billion-rupee mark in financial year 2015/16.

As for revenue growth, Browns Investments comes out on top, with a 335 percent year-on-year uptick in turnover (to Rs. 7.9 billion). Only two other LMD 100 entities – Browns Group and Lanka ORIX Leasing Company (LOLC) – reported a top line improvement in excess of 50 percent in 2015/16.

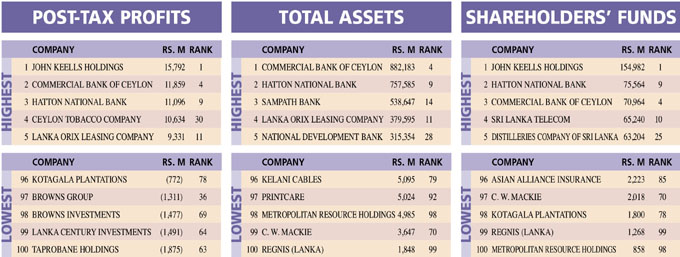

BOTTOM LINES The 2015/16 LMD 100’s cumulative post-tax profit increased by six percent versus the previous year, to record 203 billion rupees. And the profit after tax of JKH, ComBank, HNB and Ceylon Tobacco Company (CTC) also crossed the Rs. 10 billion landmark.

Meanwhile, 12 of Sri Lanka’s LMD 100 companies ended financial year 2015/16 in the red – viz. Taprobane Holdings, Lanka Century Investments, Browns Investments, Browns Group, Kotagala Plantations, Colombo Fort Land, Colombo Dockyard, Browns Capital, Lankem Ceylon, MTD Walkers, Kelani Valley Plantations and Merchant Bank of Sri Lanka & Finance – versus a count of five in the preceding year.

The big picture on the profitability front therefore, is apparently less favourable than income generation in 2015/16. Add to this equation the fact that the cumulative bottom line of the LMD 100 in 2014/15 reflected an expansion to the tune of 14 percent from the previous year, and it is clear that fortune has not favoured Sri Lanka’s listed companies in 2015/16.

In the movers and shakers space, Ceylon Grain Elevators (686%), Cargills (Ceylon) (585%), CT Holdings (222%) and E. B. Creasy (143%) lead the way from among the top 50 listed companies.

TAXATION On average, an LMD 100 entity forked out 804 million rupees in taxes for 2015/16, representing an annual hike of 25 percent from the previous year’s bill of Rs. 644 billion. On the taxation front, the future looks decidedly bleak in the aftermath of Budget 2017.

The Leaderboard accounts for 30 percent of the combined taxes of the LMD 100 in 2015/16, as the top 10’s payout rose by 20 percent (versus 5% in 2014/15), to over 24 billion rupees. And as has been the norm, CTC made the largest contribution to state coffers during the period, thanks to a Rs. 7.4 billion corporate tax charge.

ASSET VALUES The largest listed entities in Sri Lanka witnessed a substantial appreciation in asset values, with the top half of the LMD 100’s balance sheet appreciating by 19 percent from the prior year by the end of 2015/16. This top up is largely in line with the 15 percent and 16 percent uplift in asset values recorded in 2014/15 and 2013/14 respectively.

The financial services industry continues to exert its dominance in the LMD 100’s asset-related rankings, tipping the scales with a cumulative asset portfolio of nearly 4.9 trillion rupees. ComBank leads the way, with Rs. 882 billion in assets at 31 December 2015, followed by another private sector banking giant HNB (Rs. 758 billion) and Sampath Bank (Rs. 539 billion).

LAUGFS Gas comes out ahead in terms of the highest percentage gain in asset values among the top 50, with its total assets of 27 billion rupees reflecting a 77 percent appreciation from the end of the prior year. On the back of a 71 percent uplift in asset values, Textured Jersey Lanka is next in line. LOLC also joins the party by virtue of an asset base that expanded by 54 percent in 2015/16.

MOVERS AND SHAKERS Browns Group made the most notable progress in the climb up the rankings – it moves into the top 50 listed entities in 2015/16 (at No. 36), up 24 places from the preceding year. Textured Jersey Lanka also makes its presence felt, improving its standing by 10 spots (to No. 37).

In total, 22 (versus 27 in financial year 2014/15) of the island’s largest corporate entities climbed up the imposing LMD 100 ladder.

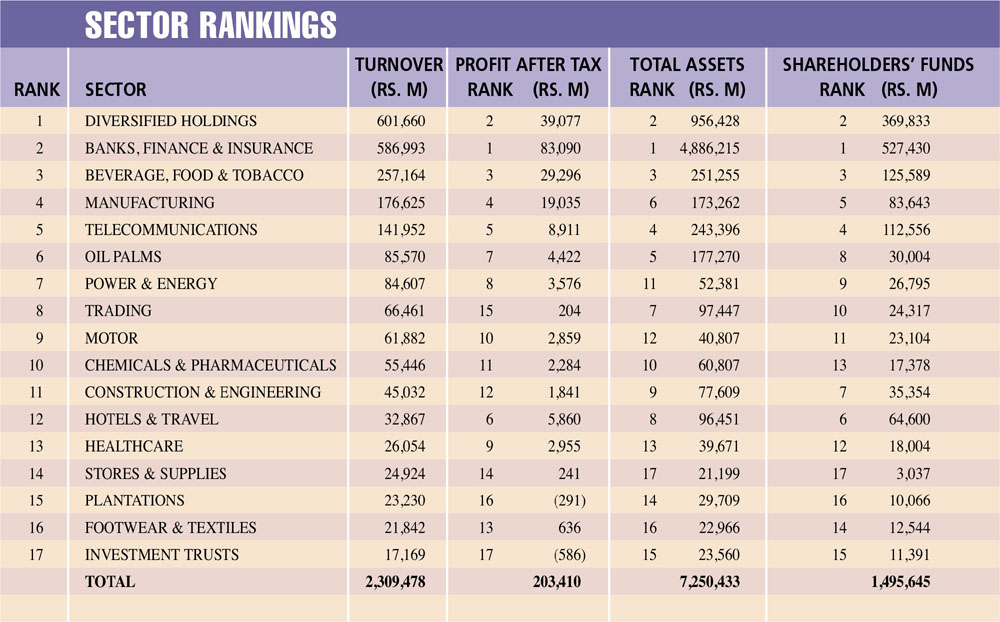

SECTOR RANKINGS The diversified holdings sector holds sway over others amongst Sri Lanka’s leading listed companies, with a cumulative turnover of Rs. 602 billion in 2015/16. This represents more than a quarter of the LMD 100’s combined income for the 12-month period.

Sri Lanka’s financial services industry is the second-largest player in the LMD 100, with an aggregate income in excess of 587 billion rupees.

The sector claims the highest contribution to total profits, asset values and shareholders’ funds in 2015/16: it accounts for 41 percent of the LMD 100’s aggregate after-tax profits, 67 percent of combined assets and slightly over a third of funds attributable to shareholders.

The island’s largest conglomerates as well as banks, finance companies and insurance firms are the lead lights among the top listed corporations in this country. Collectively, the two sectors account for more than half of the LMD 100’s cumulative turnover and bottom line.

INVESTOR YARDSTICKS CTC leads the charge, thanks to a market capitalisation of Rs. 190 billion at 31 March 2016. It is trailed by JKH, which registered a market cap of 176 billion rupees at the end of financial year 2015/16, while Nestlé Lanka and ComBank were the only other entities with a capitalisation in excess of 100 billion rupees.

In aggregate terms, the LMD 100’s combined market capitalisation declined by 11 percent (to Rs. 1,958 billion) between 1 April 2015 and 31 March 2016.

Improving on its standing in the preceding financial year, eight of the island’s 100 leading listed corporates maintained an equity value of over 50 billion rupees at the end of financial year 2015/16. And the top five (CTC, JKH, Nestlé, ComBank and Dialog) accounted for a third of the LMD 100’s market capitalisation.

THE FUTURE For Sri Lankan corporates, prospects in the year ahead will hinge on the implementation of the recently unveiled budget proposals as well as the state of the external environment following the outcome of the US presidential election, any ramifications there may be from the Brexit fallout and a world economy that continues to show little signs of turning around for the better.

In the meantime, the Ceylon Chamber of Commerce – the oldest and most influential business grouping in Sri Lanka – recently issued a communiqué welcoming the move to ease restrictions on the repatriation of export earnings.

It highlights the fact that the rule on export proceeds “would also be inconsistent with Prime Minister Ranil Wickremesinghe’s stated vision of making Sri Lanka more open and flexible to international trade and financial flows.” The chamber reiterates that the sustainable strategy to raise export earnings should be based on enhancing competitiveness through innovation and export-oriented trade, investment and macroeconomic policies.

And then there’s the world economy to contend with. The International Monetary Fund (IMF) projects global growth to slow to 3.1 percent in 2016, before recovering to 3.4 percent in 2017. Its forecast released in October has been revised down by 0.1 percentage point for 2016 and 2017 from April, which reflects “a more subdued outlook for advanced economies following the June UK vote in favour of leaving the European Union (Brexit) and weaker-than-expected growth in the United States.”

The IMF is of the view that “these developments have put further downward pressure on global interest rates, as monetary policy is now expected to remain accommodative for longer. Although the market reaction to the Brexit shock was reassuringly orderly, the ultimate impact remains very unclear.”

According to the global lending agency, “financial market sentiment toward emerging market economies has improved, with expectations of lower interest rates in advanced economies, reduced concern about China’s near-term prospects following policy support to growth and some firming of commodity prices. But prospects differ sharply across countries and regions.”

There may now be a need to revisit the world economy’s future outlook, as US President-elect Donald Trump prepares to take charge of the largest economy on Earth on 20 January 2017, given his radical proposals (on the campaign trail at least) to reinvent the wheel of American trade. The repercussions of trade renegotiations are likely to reverberate across the oceans.

Against this backdrop, emerging market and developing economies continue to face policy challenges in adjusting to commodity prices. And these prospects make the need for a broad-based policy response to bolster growth and manage vulnerabilities – spearheaded by the state, with support from the corporate sector – a matter of utmost urgency.