COVER STORY

EXCLUSIVE

THE FISCAL OUTLOOK

Manuela Goretti discusses the process of unlocking Sri Lanka’s economic potential amid the threat of global headwinds

Manuela Goretti counts more than a decade of experience at the IMF, steadily rising up the ranks from her debut as an Intern in the Research Department of the institution’s World Economic Studies Division back in 2005.

Today, she occupies the seat of Deputy Division Chief of the fund’s Asia and Pacific Department.

At the end of an IMF staff team visit in late February and in her capacity as the global lending body’s Mission Chief for Sri Lanka, Goretti emphasised that “a concerted effort is needed by all stakeholders to preserve the hard-won gains of the economic reform programme, support macroeconomic stability and strengthen the economy’s resilience to shocks.”

Sri Lanka is one of 189 countries that currently hold membership of the IMF, having joined the so-called ‘lender of last resort’ on 29 August 1950. It has a quota of SDR 413.4 million (at the end of March, one special drawing rights or SDR was the equivalent of Rs. 242), and outstanding purchases and loans in the form of standby arrangements amounting to SDR 826.8 million.

In this exclusive interview with LMD, Goretti addresses the burning issues that the Sri Lankan economy is often associated with – including the tax regime, attracting foreign direct investment (FDI), the state of state owned enterprises, currency management and the fuel pricing formula among others.

And her conclusion is that “macroeconomic stability supported by a strong policy mix and ambitious reform efforts is key to attracting long-term investors to Sri lanka.”

– LMD

Q: In a nutshell, how would you describe Sri Lanka’s country and risk profiles?

A: I would describe Sri Lanka as a country with enormous potential that has not yet been fully realised.

Sri Lanka has implemented important reforms in recent years that can foster stronger, sustainable and inclusive growth. It is essential to sustain the reform momentum to secure these hard-won gains, address the remaining macroeconomic imbalances and increase resilience to shocks.

The main risks facing Sri Lanka arise from high public debt, large refinancing needs and low external buffers. These elements make the Sri Lankan economy vulnerable to changes in global risk sentiment, a tightening in global financial conditions and other shocks.

Q: And how do you perceive Sri Lanka’s economy at present – is the lacklustre growth of recent times a cause for concern?

A: Sri Lanka needs to unlock its growth potential. To meet this objective, the government has already defined ambitious macroeconomic, structural and social reforms in Vision 2025. Consistent implementation of these reforms is a top priority to boost growth.

On the macroeconomic front, sustained efforts are needed to place public debt on a downward path; modernise monetary, financial and exchange rate frameworks; and increase international reserve buffers. And on the structural front, it’s important to gradually liberalise the trade regime and improve the business climate while promoting greater regional integration, to support investment and growth.

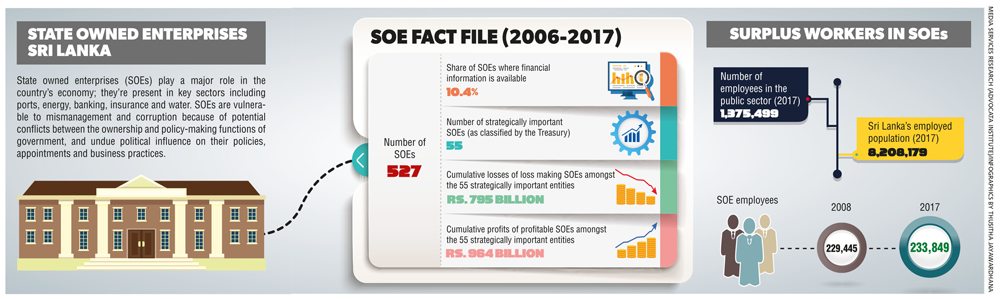

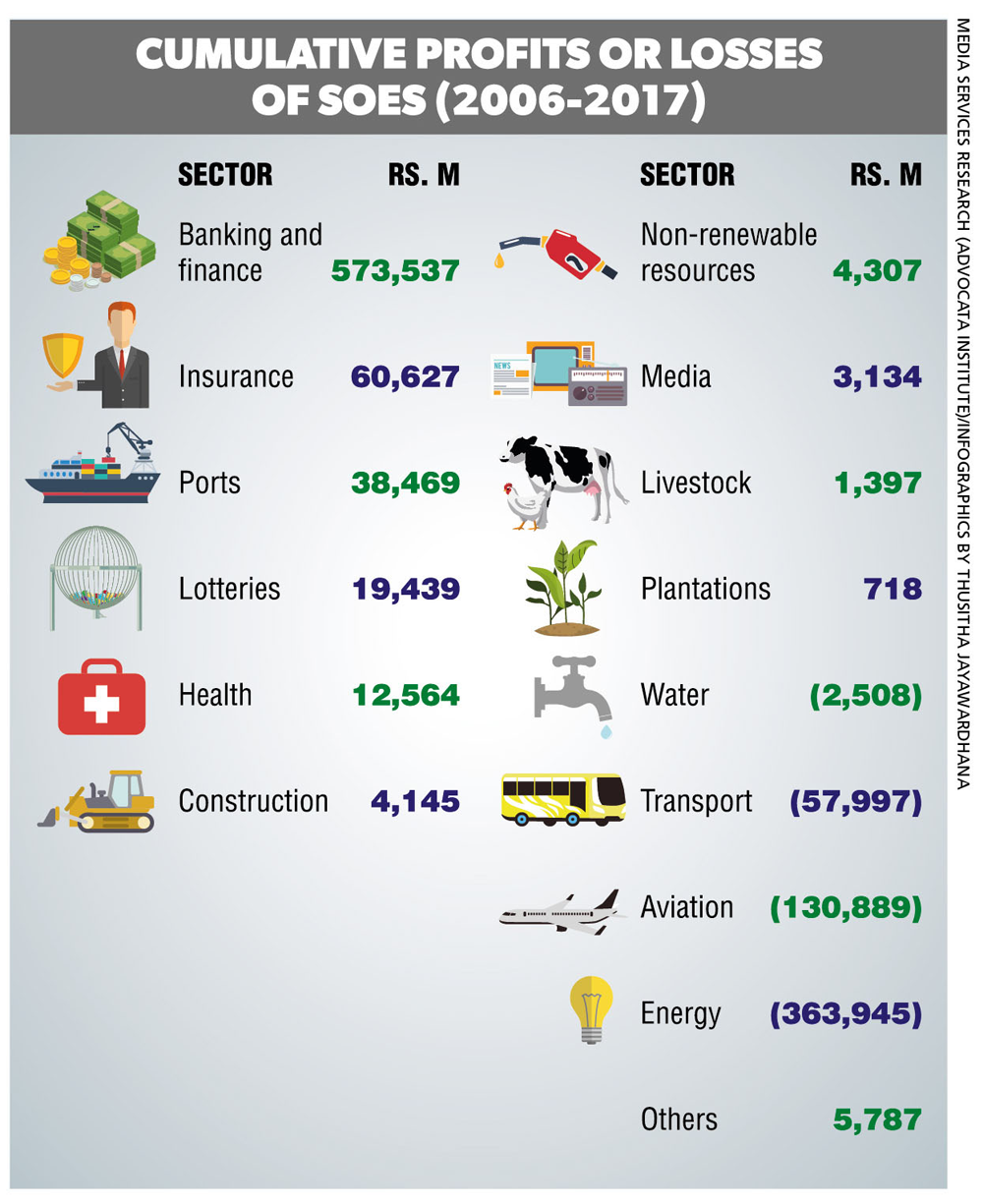

Ongoing efforts to fight corruption and strengthen institutional governance frameworks, including through greater transparency in fiscal and state owned enterprise (SOE) management, are also important.

With an ageing population, it is critical to facilitate female participation in the labour force and support the economic empowerment of women while a well-designed natural disaster crisis preparedness framework can help mitigate the impact of climate change.

Q: Has Sri Lanka made adequate progress in terms of fiscal reform as stipulated by the IMF when it granted the US$ 1.5 billion Extended Fund Facility?

A: Despite some delays in implementation, and also natural disasters and weak tax collection, Sri Lanka has made progress in fiscal consolidation under the IMF supported economic reform programme.

A: Despite some delays in implementation, and also natural disasters and weak tax collection, Sri Lanka has made progress in fiscal consolidation under the IMF supported economic reform programme.

The government reached a primary fiscal balance in 2017 and a 0.6 percent of GDP surplus in 2018.

Moreover, the introduction of the Inland Revenue Act represents a landmark reform towards a simpler and more equitable tax system, helping generate fiscal space for social and infrastructure spending in line with international best practices.

Important steps have also been taken to reduce fiscal risks stemming from state owned enterprises. For example, the implementation of an automatic fuel pricing formula has helped minimise energy subsidies that disproportionately benefitted the rich. Stronger fiscal rules, and a modern tax and customs administration, can strengthen fiscal institutions and lock in these hard-won gains.

Q: There are concerns in some quarters that reforms proposed by lending institutions such as the IMF could affect low income earners – your take on this is…?

Q: There are concerns in some quarters that reforms proposed by lending institutions such as the IMF could affect low income earners – your take on this is…?

A: When designing economic reform programmes with member countries, the IMF is very cognisant of the need to mitigate the potential short-term negative impact of reforms on the most vulnerable.

In the case of Sri Lanka, the IMF has worked together with the World Bank and the authorities in broadening the coverage of social safety nets while establishing a social registry with well-defined selection criteria to ensure that the funds reach the most vulnerable segments of the population, and thereby foster more inclusive growth.

Q: The IMF recommended fuel pricing formula has been implemented – has this met its intended purpose vis-à-vis energy pricing reforms?

A: Prior to the introduction of the formula, fuel prices were set administratively on an ad hoc basis, resulting in subsidies that disproportionately benefitted the rich and generated substantial losses for the oil company.

Formula based adjustments in fuel prices will help set retail prices at cost recovery levels while social assistance can be channelled to the most vulnerable through targeted social safety net programmes.

Q: And are we right in saying that the price of fuel should be revised downwards when there is a drop in the world market?

A: Cost recovery fuel prices would depend on the price of oil in the world market, the exchange rate, fuel tax rates and the operational cost of fuel distributors among others. If developments in these elements suggest a lower cost recovery price, the automatic pricing formula would imply that a reduction in retail fuel prices is appropriate.

Q: Do you believe that the prevailing tax regime will help achieve targets set for the local economy? And on the other hand, how do you view Sri Lanka’s competitiveness as an investment destination in the light of the nation’s tax regime?

A: Efforts to broaden the base of income tax and VAT will make Sri Lanka’s tax system more efficient, and support economic growth in the long run.

The previous income tax incentive regime with various tax holidays, profit exemptions and reduced tax rates failed to promote growth. It was replaced by the Inland Revenue Act with rule and investment based incentives designed to attract businesses with substantial upfront investment.

Sri Lanka’s business environment can also be improved by promoting predictability and transparency of income taxes, aligning them with international best practices and developing a level playing field for investors. Ultimately, macroeconomic stability supported by a strong policy mix and ambitious reform efforts, is key to attracting long-term investors to Sri Lanka.

Q: On the external trade front, how can or must Sri Lanka improve its competitiveness in the medium term?

Q: On the external trade front, how can or must Sri Lanka improve its competitiveness in the medium term?

A: Sri Lanka’s export structure has not changed in decades and remains concentrated in a few sectors. Protectionist policies such as para tariffs have hindered trade diversification. Failure to diversify exports has led to a declining share in global trade.

To remain competitive in the global market, Sri Lanka can take several measures including those outlined in the National Export Strategy, which includes creating a predictable and transparent policy and regulatory framework, driving export diversification through innovation, strengthening emerging export sectors by improving market entry and compliance capacities, and transforming into an efficient trade and logistics hub.

In addition, ongoing institutional reforms and macroeconomic stabilisation will help increase the attractiveness of Sri Lanka as an investment destination – this includes its tradable sector.

Q How can the nation attract higher levels of quality foreign investment? And what are the imperatives as far as sustaining the inflow of foreign direct investments in your opinion?

A: At less than two percent of GDP, FDI in Sri Lanka is low by international and regional standards.

Moreover, only a small fraction of FDI has reached sectors associated with global production and export networks.

A critical component of Sri Lanka’s development strategy is to attract substantial amounts of high quality FDI to a wide range of sectors in the economy. To achieve this goal, it is necessary to improve the business and investment climate by removing key obstacles identified by investors – such as barriers to market access and high tariffs – and implement the new tax system consistently.

Sri Lanka has already begun to make progress in these areas. For example, the Inland Revenue Act’s rule oriented and investment based incentives are designed to attract firms with projects involving substantial upfront investment.

In addition, it increases the predictability and transparency of income taxes, aligning them with international best practices.

Q: Is the private sector playing its part in taking the country’s economic agenda forward? What are the critical factors impeding progress in your view?

Q: Is the private sector playing its part in taking the country’s economic agenda forward? What are the critical factors impeding progress in your view?

A: Carrying a country’s economic agenda forward requires a synergy between the private and public sectors with both having distinct roles to play. It is up to the government to create an enabling environment for the private sector to thrive; and it is up to the private sector to seize investment opportunities.

In the case of Sri Lanka, the private sector has often identified a burdensome and uncertain regulatory environment as a bottleneck, which the government can help resolve.

Similarly, large-scale capital projects could be undertaken through public-private partnerships (PPPs). In this context, Sri Lanka can upgrade its PPP framework to effectively manage high return and strong governance projects, to be consistent with the country’s debt sustainability.

Q: Can state owned enterprises be turned around to make a noteworthy economic contribution – if so, how?

A: For SOEs to contribute to economic growth, their governance and transparency would need to be strengthened.

As a first important step, in 2017 the government began publishing Statements of Corporate Intent (SCIs) for five major SOEs – viz. Ceylon Petroleum Corporation (CPC), Ceylon Electricity Board (CEB), National Water Supply and Drainage Board, Airport & Aviation Services (Sri Lanka) and Sri Lanka Ports Authority.

Each SCI encompasses the SOE’s mission, a multi-year corporate plan and performance indicators, providing the basis for improved oversight and financial discipline. The SCIs can be used as a vehicle to monitor SOE performance in a transparent manner. For greater transparency, it would be important to accelerate the publication of audited financial statements, beginning with the larger SOEs.

Ongoing efforts to complete energy pricing reforms in the CPC and CEB, together with plans to restructure SriLankan Airlines, are also critical to place these entities on a sound commercial and financial footing – and thus reduce fiscal risks.

Q: What is your assessment of the prevailing monetary policy in Sri Lanka particularly in regard to currency management?

A: The Central Bank of Sri Lanka has adopted a prudent and data dependent approach to guide its monetary policy decisions, which has kept inflation broadly in line with its target. It has also enabled exchange rate flexibility in response to external shocks. These are positive steps in the road map towards inflation targeting.

Amendments to the Monetary Law Act make for a major institutional reform that will improve the decision-making structures, autonomy and accountability of the Central Bank, strengthen the legal framework for monetary policy decisions and support the adoption of an effective inflation targeting framework.

Q: And what is your take on the pace of ongoing infrastructure development?

A: Infrastructure development, if conducted properly, can be a strong building block to spur growth. Infrastructure projects should be selected and managed carefully, given the country’s high public debt and social development needs.

In this context, the importance of sound and transparent project selection cannot be overstated. It is also critical to balance the pace of infrastructure development with achieving fiscal targets. In particular, to mitigate fiscal risks, special tax treatments or gaps in financial and regulatory frameworks should be avoided.

Q: To what extent will events such as trade wars between global superpowers affect the Sri Lankan economy? And can their impact be mitigated?

A: Escalating trade tensions, and the potential shift away from a multilateral and rules based trading system, are serious threats to the global outlook.

The associated rise in policy uncertainty could undermine business and financial market sentiment, trigger financial market volatility, and slow investment and trade. Higher trade barriers would disrupt global supply chains and decelerate the spread of new technologies, ultimately lowering global productivity and welfare.

More import restrictions would also make tradable consumer goods less affordable, harming low income households disproportionately.

Sri Lanka could face spillovers from the above-mentioned risks. A possible solution to mitigate this impact would be for Sri Lanka to diversify its export products as well as partners by consistently implementing reforms to make the economy more competitive and resilient to shocks.

Q: In what ways would political instability, policy inconsistencies and corruption hinder a nation’s development especially in relation to investor confidence?

A: The IMF has always considered governance and corruption issues to play a critical role not only in harming investor confidence but also in affecting the performance of the broader economy.

In April 2018, the IMF Executive Board adopted a policy framework to help member countries address governance and corruption issues in areas that are most relevant to economic activity – namely fiscal governance, financial sector oversight, central bank governance and operations, market regulation, rule of law, and anti-money laundering and combatting the financing of terrorism (AML/CFT).

Under the IMF supported programme, Sri Lanka has made progress to support transparent fiscal management through IT based tax administration and expenditure management, integrated debt management and stringent SOE governance to mitigate corruption.

Sri Lanka has also increased efforts to strengthen its AML/CFT framework.

Leave a comment