FITCH RATINGS

Coronavirus’ Severity Will Frame Effect on Corps, Sovereigns

Fitch Ratings-New York/Hong Kong-23 January 2020: The scale of the current Wuhan coronavirus outbreak would have to increase substantially to have a significant impact on credit ratings, says Fitch Ratings. However, under such a scenario, we would expect global corporates exposed to travel and tourism to be most at risk of being affected. On the whole, Asia-Pacific sovereigns have substantial financial buffers and room for further policy easing to offset any short-term hit to economic activity from the outbreak, but their resilience to any health crisis would ultimately depend on its scale.

The new coronavirus was first identified in Wuhan China, in December 2019. It has not reached pandemic status but has sickened hundreds of individuals, some fatally, in China and internationally, according to the World Health Organization (WHO). Severe Acute Respiratory Syndrome (SARS) and Middle East Respiratory Syndrome (MERS) in 2002-2003 and 2014-2015, respectively, are also coronaviruses.

The global airlines, gaming, lodging and leisure sectors are vulnerable to pandemics that influence consumer behavior. Operational disruptions caused by idiosyncratic events – including disease outbreaks, acts of terrorism and even weather – are a perennial risk faced by these sectors. Large-scale, unpredictable events can cause immediate and severe disruptions in global travel demand that affect revenue but are typically transitory. Financial implications ultimately depend on the severity and duration of the situation.

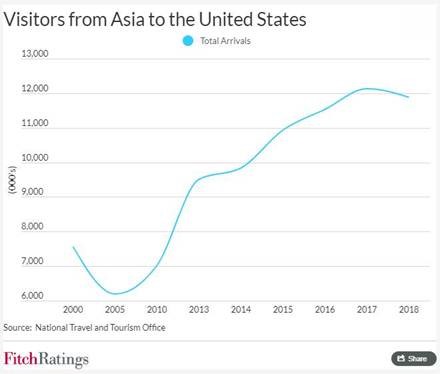

US tourism output, inclusive of lodging, transportation and reservation services, in the US alone was nearly $500 billion in 2018, with visitors from Asia rising rapidly, per data from the Bureau of Economic Analysis and National Travel and Tourism office. Tourism was equivalent to about 2.5% of US GDP in 2018.

If the Wuhan coronavirus outbreak is short lived, the shock should not result in any near-term erosion of credit metrics or negative rating actions for Fitch-rated corporates or sovereigns. If, however, the outbreak spreads and is prolonged, dampening consumer sentiment, effects could become more widespread.

Measures are being taken locally and internationally to contain the virus, including airport screenings and the quarantining of Chinese cities, including the entire city of Wuhan. Many east Asian countries have public holidays around the Lunar New Year, which starts on January 24, and normally entails hundreds of millions of people traveling, notably in China. Economic activity is normally subdued during this period. However, it could make the task of containing the outbreak more challenging.

Should the Wuhan viral outbreak escalate sharply, we believe the macroeconomic affects would initially be felt the most in Asia, where the virus originated. Service sector activity, particularly in fields associated with tourism, would be most vulnerable, which could leave economies such as Thailand, Vietnam and Singapore exposed, along with Hong Kong and Macao, both of which are already on Negative Outlook. Upward ratings momentum for Asia-Pacific sovereigns with significant tourism receipts, such as Thailand and Vietnam, where Fitch has a Positive Outlook on both, could also be affected depending on the severity of the outbreak.

Downside risks for Asian sovereigns would be mitigated by large financial buffers and easing of other macroeconomic risks. The signing of the US-China Phase One trade deal and a pause in tariffs has reduced policy uncertainty, and signs of improved activity among manufacturers and exporters in Asia are increasing. Nevertheless, for sovereigns where medium-term fiscal consolidation is a priority, such as Malaysia and Sri Lanka, there could be less room to relax fiscal policy in response to any downturn. The willingness of some authorities to use fiscal measures may be constrained by their adherence to self-imposed fiscal rules, such as in Indonesia and Vietnam, although they may have room for monetary easing in such a scenario.