BANKING SECTOR

FINANCIAL RESILIENCE

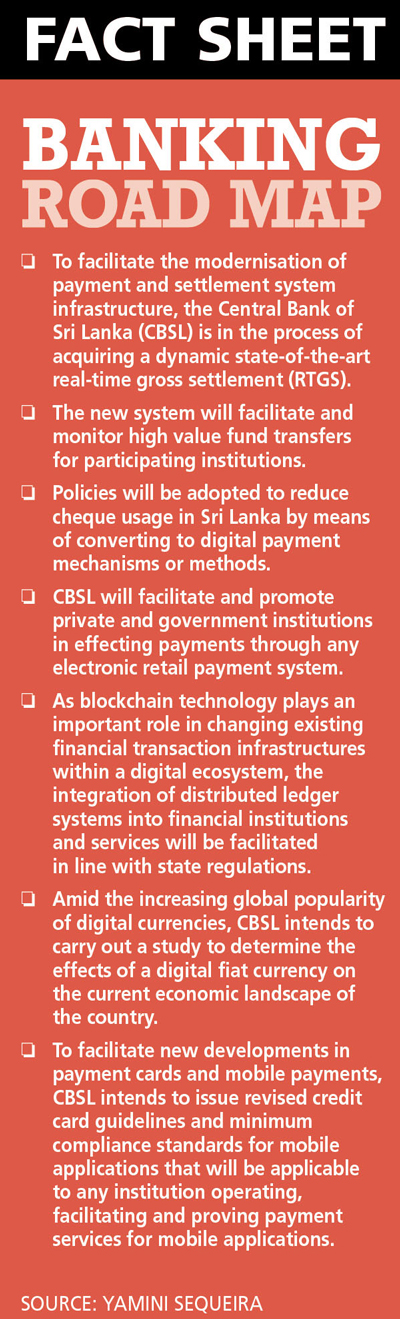

Compiled by Yamini Sequeira

STRUCTURAL SAFEGUARDS

Nimal Tillekeratne urges prudence as banks rush to digitalise operations

The banking sector’s assets exceed Rs. 10 trillion while Non-Bank Financial Institutions (NBFIs) account for over one trillion rupees. In his speech – Road Map: Monetary and Financial Sector Policies for 2018 and Beyond – delivered in January, the Governor of the Central Bank of Sri Lanka (CBSL) Dr. Indrajit Coomaraswamy outlined the clear frameworks and reforms in relation to monetary and exchange rate policies to address challenges facing the financial services industry.

Banks have been engaged in the implementation of Basel III capital standards, which is to be completed by 1 January 2019. While they have been working on improving their capital adequacy ratios, a capital conservation buffer and surcharge on systemically important domestic banks have been imposed to ensure that they actively build capital buffers.

The direction to increase existing minimum capital requirements was targeted at improving the quality of capital to ensure that these buffers are more resilient. And this is expected to safeguard the banking sector during periods of excessive credit growth and/or adverse economic conditions. It will also minimise the systemic risk arising from interconnectedness among banks.

PLAYING FIELD Chief Executive Officer of Pan Asia Banking Corporation Nimal Tillekeratne – who is also a director of the bank – observes that “the playing field in the banking sector has been redrawn in multiple areas. I see the regulator being very concerned about and focussed on basic fundamentals such as cybersecurity, good governance, anti-money laundering, capital adequacy and so on.”

But he cautions: “It’s getting tougher especially for small and medium-size banks to grow and maintain market share. The minimum capital requirements have increased three times already. By 2020, we have to comply with a minimum capital level of 20 billion rupees. This is a tough call for us all although large banks that maintain a sizeable branch footprint may sail through comfortably.”

“However, with big banks growing as fast as they are, even 20 billion rupees may not be enough in a few years,” he adds.

RATES MISMATCH CBSL has encouraged banks to slow lending by design to contain inflation. Tillekeratne sees a mismatch in deposit and lending rates, which suggests that the market is yet to warm up to the new interest rate regime. With lending growth on the decline, “banks cannot grow as fast they want to,” Tillekeratne opines, adding that consolidation and mergers will be the way forward in the years ahead.

Commenting on the past year, he remarks: “The total credit portfolio has declined for private banks. But banks are paying attention to retail where even though sizes are small, returns are high. The danger is that with so much lending in this segment, if the income patterns of the retail segment change, the impact on banks will be heavy both in terms of bad loans and the administrative costs of recovery.”

As for the presence of foreign banks in this country, Tillekeratne asserts that their performance has been good. But he points out that smaller local banks find it difficult to enter into correspondence arrangements with their parent entities.

DIGITALISATION Touching on the topic of digitalisation, Tillekeratne states: “Digital banking cannot replace bricks and mortar branches for many decades to come. This is because the culture in this country is such that there are many customers who prefer to visit branches and interact with staff. No matter the hype, digitalisation can never completely take over the customer relationship function of banks.”

He cautions that digitalisation for the sake of it is pointless. Affordability, operations applicability, accessibility and convenience should be key concerns of banks when they invest in the process of digitalisation.

“Why invest in high cost digital technology at the expense of other more pressing priorities in the short term?” asks the sector veteran who believes that banks should conduct research among target customers to assess the true potential of adopting digital banking before investing in it.

Tillekeratne avers that while digital banking could be the choice of the future, it will take time for this to become the preferred option. “Digitalisation has to come into the picture but we must remember that telcos are now entering the fintech space in a big way too!” he observes.

SMALLER ENTITIES As regards obstacles in the path of small and medium-size banks, he laments: “Entry to market is curtailed for smaller banks because large banks have additional branches in towns due to which the regulator discourages others from opening branches in the vicinity.

He continues: “The regulator is depriving us in favour of the big guns that have more than a single branch in many lucrative towns. Small and medium-size banks too need to expand and build profitable relationships in these towns.”

Elaborating on the strengths of banks, Tillekeratne avers that “the sector is highly resilient and adapts to circumstances. We have survived global financial threats and not been impacted. It’s all about the relationships that banks have with their customers.”

Meanwhile, he perceives no systemic weaknesses in the sector except that banking is over regulated: “If that were not the case, banks would invest in expanding their branch networks. The regulator should reconsider these rules – some of which are outdated.”

Even the chronic failure of finance companies isn’t a systemic issue, he maintains, adding: “But when boards and top management take the rogue route, it is usually a deliberate act and not because of systemic problems.”

BANKING OUTLOOK Commenting on the impact of increased banking activities, he says: “The economy will settle down! Micro banking is happening but you need the right business model with a strong field team.”

And he elaborates: “Every year, we witness an increase in the non-banked population entering the mainstream due to the accessibility and convenience that banks provide. Yet, there are untapped segments that need to be brought into the mainstream.”

Tillekeratne’s wish list consists of future fiscal consolidation among banks and a lower cost of banking.

He is unequivocal in his view that investing in training and developing people will render service levels a key differentiator in the banking arena.

Looking ahead, he feels that 2018 will be fruitful if current fiscal and monetary policies remain as they are. SMEs and retail cannot survive without government inputs, he concludes.